Written Commentary

Overnight trade has SRW Wheat up roughly 4 cents; HRW up 4; HRS Wheat up 5, Corn is up 7 to 1 cent; Soybeans up 9 to 1; Soymeal up $0.50, and Soyoil up 45 to 30 points.

Chinese Ag futures (September) settled down 4 yuan in soybeans, up 2 in Corn, down 18 in Soymeal, down 2 in Soyoil, and up 74 in Palm Oil.

Malaysian palm oil prices were closed for holiday.

U.S. Weather Forecast: Both last evening’s GFS model run and the midday GFS model run showed significant precipitation in the Northern Plains May 8 – 10.

South America Weather Forecast: Notable moisture relief to interior southern Safrinha corn areas of Brazil is still unlikely in at least the next two weeks and last evening’s GFS model run kept much of this area mostly dry. Conditions in Argentina will still be favorably mixed the next two weeks.

The player sheet had funds net sellers of 10,000 contracts of SRW Wheat; net sold 40,000 contracts of Corn; sold 7,000 Soybeans; sold 4,000 Soymeal, and; net even in Soyoil.

We estimate Managed Money net long 35,000 contracts of SRW Wheat; net long 494,000 Corn; net long 204,000 Soybeans; long 50,000t Soymeal, and; net long 118,000 Soyoil.

Preliminary Open Interest saw SRW Wheat futures up roughly 1,000 contracts; HRW Wheat down 735; Corn down 26,800; Soybeans down 28,300 contracts; Soymeal down 5,900 lots, and; Soyoil down 1,000.

There were no changes in registrations—Registrations total 10 contracts for SRW Wheat; ZERO Oats; Corn ZERO; Soybeans ZERO; Soyoil 968 lots; Soymeal 175; Rice 1,013; HRW Wheat 1,291, and; HRS 235.

Tender Activity—Philippines seek 185,000t optional-origin wheat—Algeria bought an estimated 200,000t to 360,000t optional-origin wheat—S. Korea feed groups bought 271,000t optional-origin corn; seek 138,000t optional-origin corn—Egypt bought 30,000t optional-origin soyoil—

For the week ended Apr 23rd, ethanol production was 945,000 barrels per day, up 0.43% versus a week ago, up 76% versus a year ago. Stocks were 19.7 mil barrels, down 3.5% versus last week, down 25.0% versus last year. Corn used was 95.5 mil bu versus 95.1 mil last week and versus the 97.4 mil needed to meet USDA projections.

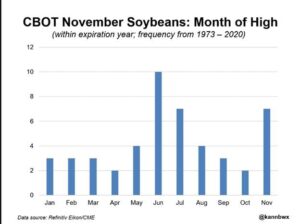

Wire story report had price action for corn and soybeans on the Chicago Board of Trade has been nothing short of impressive this month, and more could be in store for the new-crop contracts as April is historically an uncommon time for their high-water marks. Since 1973, new-crop November soybeans have made their annual highs in April only twice: 1986 and 1981. Along with October, April is the least common month for the high. December is not considered here since the analysis examines the only the year of expiration. June is the most popular month for highs in new-crop soybeans with 10 instances in the last 48 years. July and November are tied for second with seven apiece. May and August are next at four each.

Wintery weather delays early U.S. corn sowings – Refinitiv Commodities Research

—2021/22 US CORN PRODUCTION: 389 [353–429] MILLION TONS

—With cold weather putting a halt to the rapid sowing pace seen earlier in the month, unchanged area and yield forecasts maintain 2021/22 U.S. corn production at 15.32 [13.9–16.9] billion bushels. Corn area is still expected at 93.9 million acres, above the USDA March Prospective Plantings report figure of 91.4 million acres. The next USDA survey-based estimate of acreage will be released in the 30 June Acreage report.

When Microsoft Corp made a massive purchase of carbon credits in January, it turned to a relatively new source: farmers who plant crops meant to trap carbon in the soil. The credits are financial instruments generated by projects that reduce or avoid the release of greenhouse gases, such as solar farms or tree-plantings. The projects’ owners can sell the credits to companies who then use them to make claims of offsetting the climate impact of their operations. Microsoft bought nearly 200,000 of the farm-based credits at an undisclosed price – among the largest-ever purchases of agricultural credits – as part of a larger deal to buy 1.3 million credits. But the tech giant rejected far more of the more than 5 million credits offered by agriculture projects because of systemic problems with measuring their climate benefit. The Microsoft purchase underscores both the promise and the problems of the emerging industry in agriculture-based climate credits.

Brazil’s second corn crop conditions continue to decline – Refinitiv Commodities Research

—2020/21 BRAZIL CORN PRODUCTION: 104.7 [95.0–109] MILLION Tons, down <1% from last update

—Despite favorable conditions in the northern Center West and a slight uptick in expected first crop yields, persistent dryness in southern second crop areas lowers 2020/21 total Brazil corn production to 104.7 [95-09] million tons. Total corn area is still seen at 19.0 million hectares, still 0.7 million hectares below USDA’s World Agricultural Outlook Board (WAOB) figure from April, which maintained total corn sowings at 19.7 million hectares and national-level yield of 5.53 tons per hectare.

Vegetation density indicates small upsides to Brazil’s soybean crop – Refinitiv Commodities Research

—Updated satellite imagery suggests yield upsides to minor, later-sown areas, fractionally raising Brazil’s 2020/21 soybean production to 132.4 million tons as harvests are nearing completion. The outlook is now 3.6 million tons below USA’s World Agricultural Outlook Board (WAOB) estimate released in April, which has sowings at 38.6 million hectares and production at 136 million tons, up two million tons from March. Brazil’s agriculture state agency (CONAB) in its April outlook raised expected yields and pushed production up fractionally to 135.5 million tons.

Argentina’s stalled soy harvest is set for a boost from a period of expected dry weather, meteorologists and grains analysts said, after recent heavy rains in key farming areas had slowed down farmers gathering in their crops. The expected weeks of dry weather should help allay fears of further losses to the important soy harvest in the world’s largest exporter of processed soy meal and oil, which relies heavily on the grain for much-needed foreign currency.

Argentine farmers have sold 15.53 million tonnes of 2020/21 soybeans, after registering 1.16 million tonnes in the most recent reported week period, the Ministry of Agriculture said. The ministry said that the rhythm of sales was behind the previous cycle a year earlier, when at the same date it had registered sales of 20.26 million tonnes of soybeans. Argentine farmers are clinging to their crops, despite a high international price, as a hedge against a weak local peso currency, weighing on the flow of export dollars the country needs to replenish its battered foreign currency reserves.

The dredging of the Parana River, Argentina’s grains superhighway, will continue for another 90 days, according to a government resolution issued on Wednesday aimed at ensuring that the country’s export hub of Rosario will stay open for business. The current dredging contract was set to expire at the end of the month. The looming deadline had caused nervousness in the local grains industry, the country’s main source of export dollars, at a time when central bank reserves are being strained by a three-year recession exacerbated by the COVID-19 pandemic. “It’s official. This guarantees the maintenance of the river. The current system will continue for another 90 days.

Paraguay soybean production lowered fractionally, as dry conditions in Alto Paraná continue – Refinitiv Commodities Research

—2020/21 Paraguay soybean production: 9.9 [9.0–10.2] million tons, down <1% from last update

Russia is considering reducing its export tax on soybeans to 20%, but not to less than $100 per tonne, starting from July 1, the Interfax news agency reported. Russia’s export tax on soybeans is set at 30%, with a minimum level of 165 euros ($199) per tonne, until June 30.

Ukraine’s 2020/21 season corn ending stocks could reach a record 2.7 million tonnes, or 70% more than a season earlier, the APK-Inform agriculture consultancy said. Ukraine harvested 30.3 million tonnes of corn in 2020 and the consultancy forecast that the exports might total 23.2 million tonnes.

Such a significant volume of carry-over corn stocks should have an overwhelming effect on price dynamics. However, limited farmers’ corn supplies to the market is still supporting an upward price trend. The consultancy said this week corn bid export prices rose by $7 over the past week to $262-$267 FOB.

Ukraine is likely to increase its wheat harvest by 9.5% to 27.7 million tonnes in 2021 and the higher output could allow it to boost wheat exports to 21 million tonnes in the 2021/22 July-June season, Ukrainian grain traders union UGA said on Thursday. The union said Ukraine could also harvest 35.5 million tonnes of corn and 8.2 million tonnes of barley. The corn exports might reach 30 million tonnes next season, while barley shipments may total 4.2 million tonnes.

Euronext wheat ended slightly lower on Wednesday, recovering from an earlier slide in step with Chicago as grain markets sought fresh direction after a steep rally this month. September milling wheat settled down 0.75 euros, or 0.3%, at 226.75 euros ($274.14) a tonne. In earlier lost as much as 7.25 euros as it retreated from Tuesday’s life-of-contract high of 233.50 euros.

High expected profitability and long-rang weather outlooks set Australia wheat production at 27 mmt – Refinitiv Commodities Research

South Africa corn production boosted by the latest satellite imagery – Refinitiv Commodities Research

Egypt’s strategic reserves of vegetable oils are sufficient until September following the latest purchase by its General Authority for Supply Commodities on Wednesday, the supply ministry said.

Indonesia March crude palm oil output, exports surge on-year – Reuters News

Indonesia’s crude palm oil production and exports surged in March on-year, while end-stocks remained low, signalling prospects of higher prices in the near future, an official at the country’s palm oil association GAPKI said on Wednesday. Crude palm oil output stood at 3.71 million tonnes in March, 13.5% higher than the 3.27 million tonnes produced in the year-ago period, and up 20.9% compared with the previous month. Palm exports, including refined products from the top producer, stood at 3.24 million tonnes in March, up 18.68% from a year ago and 62.8% higher from February.