Written Commentary

>>Read the full September 2024 Edition HERE

Prices remain range bound between $4.00 – $4.15 for spot December 2024 futures. Strong demand and speculative buying are generating support. There has been a significant reduction of speculative shorts in the marketplace. Farmer selling and the outlook for record U.S. yields have limited the upside. U.S. production in September was increased 39 mil. bu. to 15.186 bil., 30 mil. above expectations. Record yields at 183.6 bpa, were up from 183.1 in August. Old crop ending stocks were trimmed 55 mil. bu. to 1.812 bil., roughly 40 mil. below expectations. Exports were raised 40 mil., while usage for ethanol was increased 15 mil. There were no changes to the new crop usage figures, leaving ending stocks at 2.057 bil., nearly 50 mil. above the average trade guess.

November soybeans are grinding sideways in a $9.95 – $10.30 trading range. I would not expect this to last much longer. U.S. production was cut 3 mil. bu. in September to 4.586 bil., nearly 25 mil. below expectations. Record yields were left unchanged at 53.2 bpa. Old crop stocks were cut 5 mil. to 340 mil., which was in line with expectations as a result of the higher crush. New crop stocks were cut 10 mil. bu. to 550 mil., approximately 35 mil. below expectations. The USDA raised the amount of bean oil used in biofuel production by 100 mil. lbs. to 13.0 bil., which was back where it was in July. Global stocks were little changed at 134.6 mmt, which was in line with expectations.

The USDA made no changes to the 24/25 balance sheet with ending stocks left at 828 mil. bu. We were expecting a 20 mil. bu. drop on higher exports. There will be no U.S. production changes until the end of September in the Small Grains Annual Summary. 2024/25 global stocks at 257.2 mmt were slightly above expectations. Production was cut 4 mmt in the EU to 124 mmt, which was offset by at 2 mmt increase in Australia and a .7 mmt increase in Ukraine. A recent Russian missile attack on a Ukrainian vessel carrying wheat to Egypt triggered a wheat rally at mid-month. Prices quickly fell back as tensions cooled. Headlines from the Ukraine/Russia war will continue to drive price volatility.

Cattle trading slowed in August. It was the dog days of summer. Besides the heat when cooks do not want large roasts in hot oven, they are paying off the summer vacation credit card bills and the expenses of kids going back to school. Beef sales are slow and so is demand for cattle. Cattle prices peaked the last week of July and began to fall the first week of August.

Lean hog prices from April 2024 through the second week of July dropped close to $20.00. There was a recovery in July of approximately $10.00 but by August hog and pork prices began to drift lower. The main reason for the lower prices is the larger inventory of hogs in 2024 on top of increasing hog numbers in 2023. As of August 30, 2024, U.S. federal hog slaughter was 1,063,779 hogs more than the same time in 2023. However, slaughter in August 2023 was also higher by 1,132,000 hogs compared to 2022. On August 1, 2024 the CME hog index was $93.64, by July 15 it was $90.09, and by August 30 it was down to $86.15.

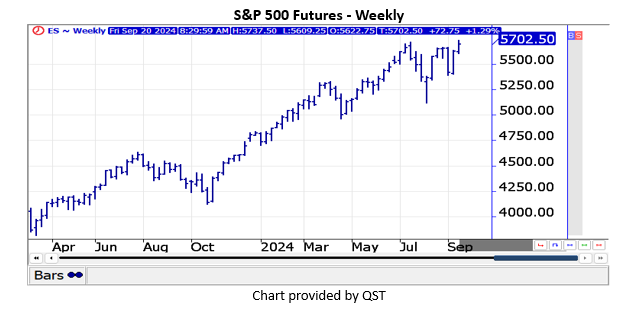

S&P 500 and Dow Jones futures advanced to new record highs after the Federal Open Market Committee decided to lower its fed funds rate by 50 basis points to 4.75% – 5.00%. A majority of analysts expected the FOMC to lower its fed funds rate by a half-point, although there was a minority view that the FOMC could reduce its key interest rate by only 25 basis points.

The Federal Reserve’s pivot to accommodation was the first rate cut since March 2020. Federal Reserve Chair Powell said the central bank is not in a rush to ease policy and that half-percentage point cuts are not the “new pace.”

The U.S. dollar index declined to its lowest level since December of 2023 after the FOMC reduced its key interest rate by 50 basis points. However, there has been a recovery on the belief that other central banks will be lowering their key rates as well, which tends to mitigate the bearish differential expectation that has undermined the dollar index since early July through mid-September.

The euro currency trended higher in August but has traded In a broad sideways trend in September. There has been overhead resistance for the euro after a recent report that showed a sharp drop in investor confidence in the euro zone and a surprising decline in industrial activity. Euro area gross domestic product increased 0.3% in the second quarter, which is unchanged from the previous quarter and matched preliminary estimates. The potential for an additional interest rate reduction from the European Central Bank may limit the upside for the currency of the euro zone.

December crude oil futures trended higher in the last two weeks, driven by potential supply risks in light of rising Middle East tensions, which could disrupt crude supplies.

In addition, there has been support following the Federal Reserve’s 50 basis-point reduction in its fed funds rate at its September 18 policy meeting, which could stimulate economic activity and improve the outlook for U.S. energy consumption.

GOLD

December gold futures advanced to new record highs after the Federal Open Market Committee announced it decided to lower its fed funds rate by 50 basis points to 4.75% – 5.00%. This is the first rate cut since March 2020.

The Federal Open Market Committee released its economic projections at its September 18 meeting. The unemployment rate projection for 2024 was increased from 4.0% to 4.4%. The PCE inflation projection was lowered from 2.6% to 2.3%, and the Core PCE inflation projection was reduced from 2.8% to 2.6%.

Interested in more futures market commentary? Explore our Market Dashboards here.