Written Commentary

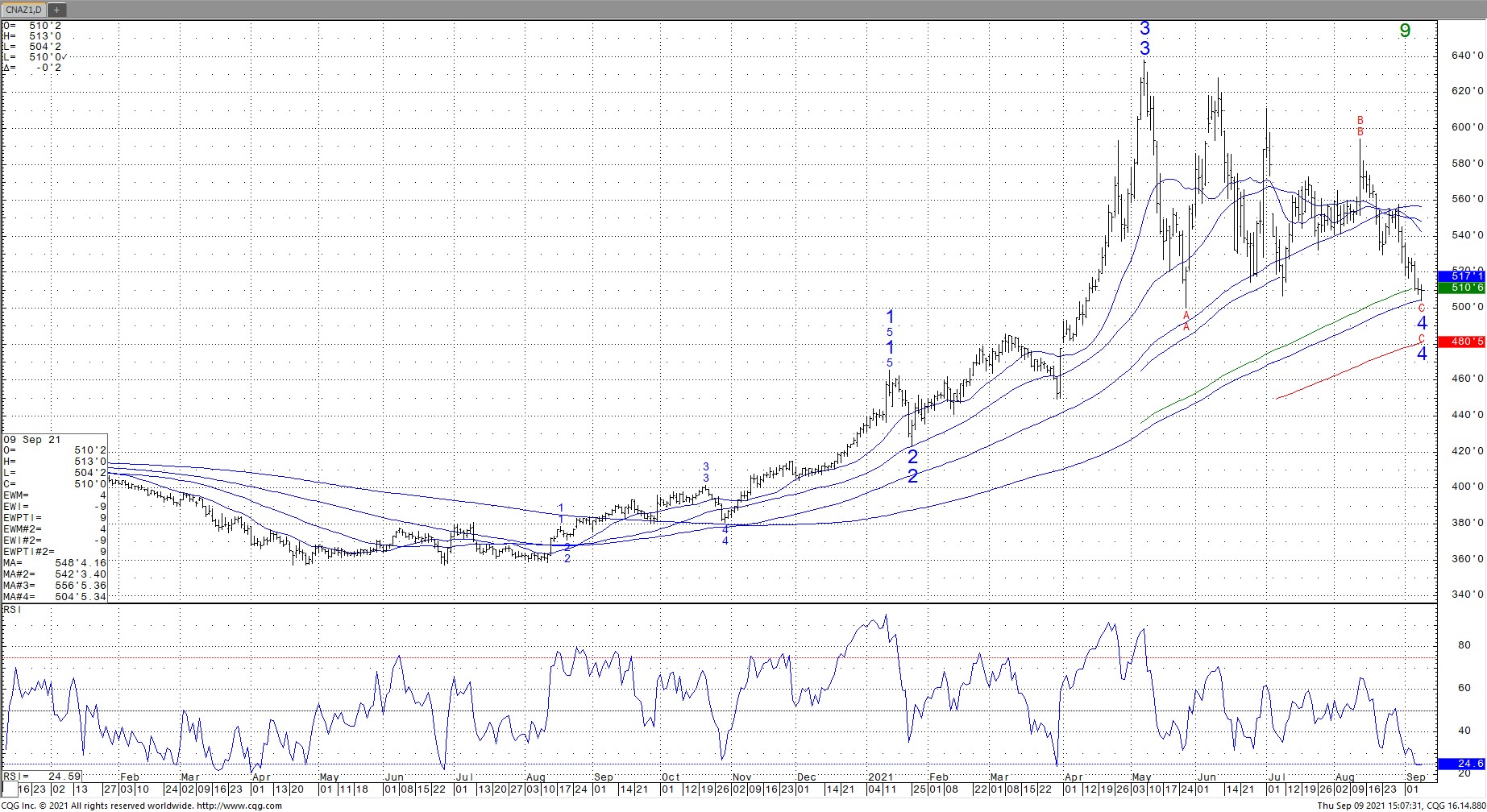

SOYBEANS

Soybeans and soyoil ended lower. There is concern that tomorrow USDA might increase US 2021 soybean acres, yield and crop size. They could also lower US 20/21 soybean total use. This could add to US 21/22 soybean carryout. Ongoing lack of US gulf exports has also weighed on soybean futures. There is talk that a few of the gulf elevators may have or soon will get power. This will give them time to access damages and begin repairs. Weekly US soybean export sales are est near 1,000-1,600 mt vs 2,132 last week. USDA announced 132 mt new sales to China. There was also talk that they may have bought another 300 mt overnight. Brazil 2 week forecast is dry and warm for soybean planting. Some are estimating Brazil 2022 crop near 144 mmt vs 137 this year and Argentina 51 mmt vs 46. Matif and China Dalian rapeseed futures traded higher on concern about Canada supplies. Soyoil dropped on talk China may sell soyoil from reserves. Trade est US 2021 soybean crop near 4,377 mil bu vs USDA 4,339 and 21/22 carryout near 190 vs USDA 155.

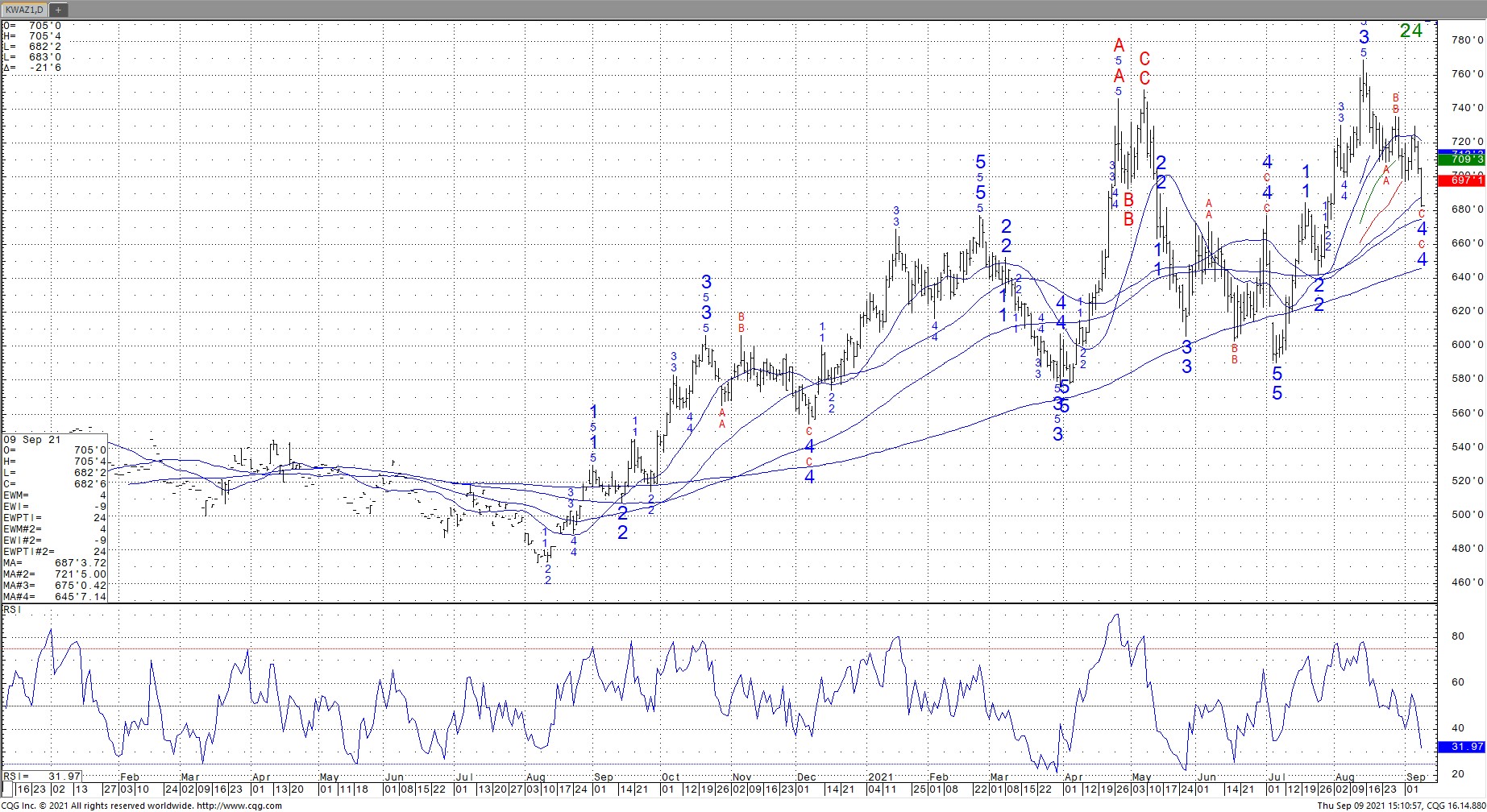

CORN

Corn futures ended unchanged. CZ ended near 5.10 with a range of 5.04 to 5.13. Corn bounced off session lows on talk a few US gulf elevators may have or will soon get power back. This could allow them to access damage and begin repairs. US cif and barge market saw an uptick on the news. Most of the drop from the August crop report was linked to a slowdown in new US corn export demand especially by China. China Dalian corn futures made new lows overnight. Weekly US corn export sales are estimated near 600-1,200 mt vs 1,159 last week. Last week China corn open sales were near 10.7 mmt with 1.8 in unknown. Last year China took 23 mmt of US corn. Commercials feel China will take another 23 mmt in 21/22 from the US. USDA FSA released their latest est of US acres enrolled in farm programs. The numbers suggest USDA could increase US 2021 corn and sorghum acres on tomorrows report. They usually use the data for the October report. Quicker data collection allowed them to use the data tomorrow. Trade est US corn crop near 14,492 mil bu vs USDA 14,750. Trade could also see USDA increase 20/21 corn carryout to 1,169 from 1,117 due to lower domestic use. Trade could also see USDA increase US 21/22 corn carryout from 1,242 mil bu to 1,382. Weekly US ethanol production was up from last week but still below last year. Stocks were down from last week but up from last year.

WHEAT

Wheat futures ended sharply lower as Managed funds liquidate their net long positions in front of USDA September report and the end of the 2020/21 season and the start if the 2021/22 season. Wheat futures broke below key support levels which increase chart pattern selling. Managed funds have now rolled out of a net Chicago long to a new net short. Weekly US wheat export sales are estimated near 200-450 mt vs 295 last week. US sales pace is behind ;ast year and USDA est exports to be near 875 mil bu down from 992 last year. Some talk that US HRW plantings are starting favorable due to recent rains may have also weighed on futures. This despite forecast that La Nina suggest drier US south plains 2022 weather. Some est that in 2022, US, Canada, EU and Russia crops could rebound to closer to 305 mmt vs 275 this year.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.