Written Commentary

SOYBEANS

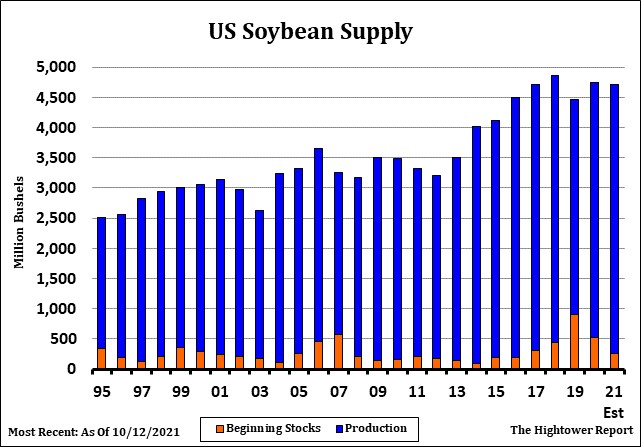

Soybeans traded lower. Failure for SX to trade over 12.50 and the long term lower trend line of resistance triggered new selling. There was talk that China may import less US Ag goods due to slower economy. There was also fears that there may not be a Phase 2 deal between US and China. This could limit China buying to what they need versus based on trade agreement. Managed funds were net sellers of 12,000 soybean contracts, 2,000 soymeal and 6,000 soyoil after buying 11,000 soybean, 4,000 soymeal and 8,000 soyoil on Wednesday. Dalian soyoil, palmoil and rapeoil futures made new highs on talk of higher demand. Weekly US soybean export sales were 2.87 mmt and 4th largest on record. Some might say recent rally may he been due to these sales. Now what? Total commit is near 29.3 mmt vs 45.3 ly. USDA goal is 56.9 mmt vs 61.7 ly. China sales were 1.9 mmt. China commit is 14.9 mmt with 7.3 in unknown. Will China take 30 mmt? Brazil weather remains favorable. Argentina is dry. Soybean futures may be under pressure if US 2021/22 carryout increases and there is a need for less US 2022 acres.

CORN

Corn futures traded lower. Failure for CZ to trade over 5.40 triggered new selling. There was talk that China may import less US Ag goods due to slower economy. There was also fears that there may not be a Phase 2 deal between US and China. This could limit China buying to what they need versus based

on trade agreement. Managed funds were net sellers of 8,000 corn contracts after buying 9,000 on Wednesday. Dalian, Matif and Black Sea corn futures traded higher on talk of tight supplies. US farmer increased cash sales. Weekly US corn export sales were 1.27 mmt. Some might say recent rally may

have been due to these sales. Total commit is near 28.9 mmt vs 28.3 ly. USDA goal is 63.5 mmt vs 69.9 ly. China commit is 11.9 mmt with 2.5 in unknown. Will China take 20 mmt or 14? Some of the unknown could be to Canada. Brazil weather remains favorable. Argentina is dry. Some fear US farmers may plant lees corn acres on 2022 due to higher cost of planting. NOAA 3 month warm and dry weather forecast triggered selling in energy futures corn. Supply chain issues could push finished product prices higher and reduce food and fuel demand. This weeks US ethanol data suggested US corn use could increase 100 mil bu vs USDA guess.

WHEAT

Wheat futures ended lower. WZ was near 7.41. KWZ was near 7.48. MEZ was near 9.85. Managed funds were net sellers of 6,000 Chicago wheat contracts vs buying 9,000 on Wednesday. Some feared that wheat futures had become overbought and due for a correction. Matif wheat futures made new highs on supply concerns. EU wheat exports continue to exceed supply. Some feed wheat is being sold to China. Russia wheat prices continue to trend higher on higher export tax. Russia continues to tr to export wheat before Jan 1 wheat export quotas. There was talk that Ukraine wheat exports could reach 25 mmt vs USDA 23. NOAA 30 an 90 day US south plains forecast calls for above temps and below rains. Weekly US wheat export sales were only 392 mt. Total commit is near 12.3 mmt vs 15.4 last year. USDA goal is 23.8 mmt of World total of 199.6 vs 27.0 last year. Last years World trade was 200.3. Failure of WZ to test or trade over 7.60 could suggest a test of 7.00. This week, Informa est US 2022 wheat acres at 48.8 mil vs 46.7 ly and a crop of 2,059 mil bu vs 1,646 this past year.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.