Written Commentary

SOYBEANS

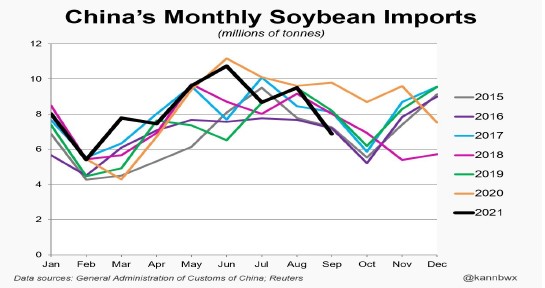

Soybeans ended higher. New tech related buying helped SX bounce off this weeks lows. Weekly soybean range 12.02 to 12.21. This was the 9th straight week of lower closes since early August. USDA NASS admitted that Sep 1 stocks were higher than expected which forced them to raise the 2020 crop. Not the other way around? China came back to US soybean market. USDA announced today 396 mt US soybeans to unknown, 326 mt previous soybean sales sold to unknown and 132 mt US soybeans to China. Weekly US soybean exports sales were near 42 mil bu. Total commit is near 969 mil bu vs 1,584. Metric tonnes is 26.4 mmt vs 43.1 last year. China soybean export commit is near 13.0 with 6.7 in unknown. Will they take 30 mmt? US Sep NOPA soybean crush was 153.8 mil bu vs 158.8 in August and at 3 month lows. Last years crush was 161.5. End of Sep NOPA soyoil stocks were 1,684 mil lns vs 1,668 in August. Most estimate US soybean harvest near 65 pct vs 49 last week. Rains in Brazil and Argentina is helping crops there off to a good start. Forecast of dry weather in Argentina could stress crop there later. World rapeseed prices continue to trade higher on lower Canada crop.

CORN

Corn futures traded higher. Tech related buying offered support. For the first time in 5 week. Nearby corn futures had a lower weekly close. Weekly range was 5.14 to 5.28. Key will be If next week CZ can trade over 5.33 and the high before USDA October report. USDA NASS said they could still adjust US 2021 corn acres based on final FSA acres. Some feel US corn harvest is near 55 pct done vs 41 last week. Latest yields have been trending higher. French corn harvest is near 15 pct vs 62 last year. Corn yields have also been trending higher. Weekly US ethanol production was up from last week and last year. Stocks were down slightly from last week and last year. Margins remain positive. Processors continue to reach for ownership. Ukraine harvest is near 22 pct done. Ukraine corn yields also trending higher. China announced they will begin to auction wheat from reserves. This could suggest a lower feed supply. Brazil corn plantings is advancing under favorable weather. Argentina also raised their corn G/E rating 3 pct to 27. Weekly US corn exports sales were near 41 mil bu. Total commit is near 1,087 mil bu vs 1,043. Metric tonnes is 27.6 mmt vs 26.5 last year. China corn export commit is near 11.9 with 2.1 in unknown. Will they take 14 mmt or 20? Post US 2021 crop harvest trade attention will turn toward new export demand and South America weather. USDA est Brazil 2022 corn crop near 118 mmt vs 86 this past year. They also est Argentina crop near 53 mmt vs 50 this past year. Attention will also focus on US cost to plant the 2022 corn crop. C IL NH3 cost has been quoted near $1,200. Ukraine announced switch to barley and sunseed acres from corn due to high cost of planting.

WHEAT

Wheat futures ended higher. WZ was near 7.24. KWZ ended near 7.37. MWZ ended near 9.60. Nearby Chicago wheat closed lower this week for the first time in 5 weeks. Some thought that US futures were overbought. Others thought EU wheat futures were also overbought. USDA October crop report was friendly. USDA lowered US 2021/22 wheat carryout below 600 mil bu for the first time in 8 years. USDSA also estimated World wheat exporters stocks to use ratio at record low. Some also feel La Nina could lower US 2022 south plains rainfall. Weekly US wheat exports sales were near 21 mil bu. Total commit is near 440 mil bu vs 553. Metric tonnes is 11.9 mmt vs 15.0 last year. US HRW export prices are competitive for buyers in 2022. Most look for a slowdown in EU and Russia exports to help demand for US. MWZ continues to make new highs on record low World milling wheat supplies. China buying EU wheat is supportive. There are rumors they may have bought a cargo of US SRW.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.