Written Commentary

SOYBEANS

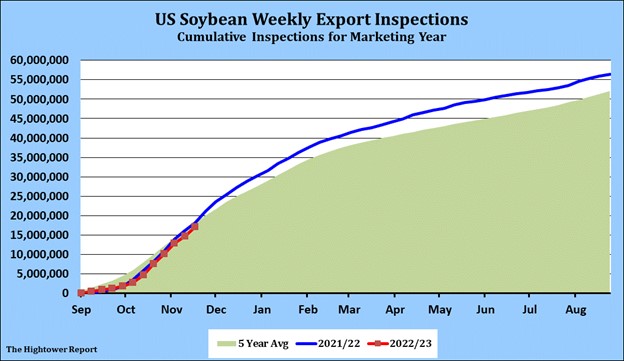

Soybean futures ended higher. SF continues to trade between 14.00 and 14.50. Resistance comes from talk that China reported first Covid deaths in 6 months. There is also talk that 3 key cities may be in lockdown. Soybean futures were on the defensive until Saudi Arabia denied they were going to increase Crude oil prediction Crude oil rallied from $75 to $79 quickly and soyoil and soybean followed. Our weather guy feels that actual rainfall in parts of S Brazil and S Argentina may be less that forecast. Still Brazil February price are 85 cents below US. Weekly US soybean exports were near 85 mil bu. Season todate exports are 629 mil vs 703 ly. Some feel final exports could be 65 mil bu below USDA est of 2,045.

CORN

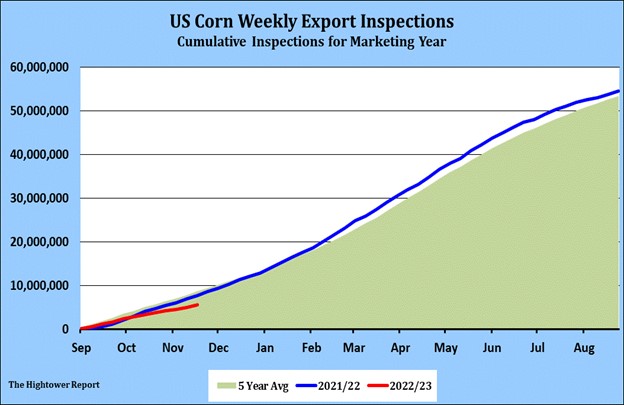

Like wheat, Matif corn reversed to a near unchanged close following the 5 pct rebound in crude. Just one more example of the extent to which algorithms and order flow spill across all markets. Ukraine has harvested just 50 pct of this year’s planted acreage, equating to 12.3 mmt according to the Ag Min with snow now falling. Most of the remaining acreage is expected to stay in the fields until spring. And that asks some additional important questions about next year’s Ukraine corn crop. If by next Apr-May, 50 pct of the acreage still has last year’s crop on it, how much of the 2023 crop will they realistically plant? And with no cash flow due to rock bottom prices, plus huge fertilizer costs, where should next year’s yield be put? Many US traders say this will not be an issue as the war will be over by then. Some disagree. Weekly US corn export were near 19 mil bu. Season to date exports are 215 mil bu vs 308 last year. Most still look for final US exports to be closer to 2,000 mil bu vs USDA 2,150. Some are plugging in record 2023 Brazil corn crop which that and Ukraine exports could reduce final US exports. US feeder and crush basis remains strong. Possible US RR strike could break basis lower. US Miss river levels are beginning to drop again.

WHEAT

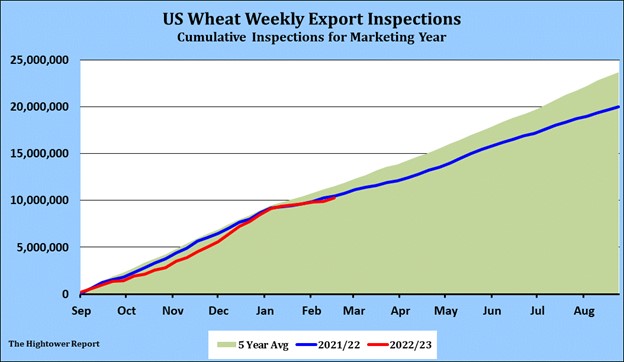

Matif closed slightly higher after crude reversed on Saudi denials of an output increase. Polish wheat remained at a huge discount into the US, with several cargoes now confirmed into Florida and more being worked. GASC bought another 60 mt last Friday taking their season total through Jan to 3.5 mmt. Algeria is back Thursday for Dec-Jan durum wheat. Ideas on Black Sea Fob values remain in a wide range, but we would call the sell side of Russian 12.5 pro at $320, with 11.5 pro a $10-15 discount and feed wheat a further $25-30 lower, whilst Balkan wheat continues to command a premium of around $20 over Russian. Russia has not officially confirmed the extension of the corridor and there is no news on the lifting of sanctions on Rosselkhozbank but assuming a mild winter, combined Russian-Ukraine export capability is now pushing 60 mmt. Rain continues across those southern European areas that need it mos. E Ukraine and S Russia have no snow cover with temperatures still well above normal. Weekly US exports were 10 mil bu with season to date exports 372 vs 386 ly.

See more market commentary here.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.