Written Commentary

Old crop soybeans, soymeal, soyoil and wheat traded lower. New crop soybeans and corn managed gains.

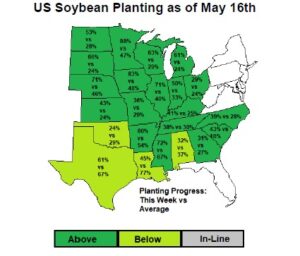

SN traded lower on talk that 16.00 may have ration US demand. US soybean exports have slowed and NOPA crush was lower than expected. Lower crush supported soyoil futures. There remain some concern over Asia vegoil demand especially in India where virus continues to spread. Support had been found earlier on talk that USDA 23 mmt increase in World 2021/22 soybean crop offered resistance. Still, these numbers include record 2022 Brazil soybean acres and yield. It also include record US 2021 acres and yield. Finally it includes 3 pct increase in Argentina 2022 acres and 7 pct increase in yield. This might be optimistic. US soybean planting was reported at 61 pct vs 37 average. Soybean planting was most behind in LA (45 vs 7 avg). Soybean planting was most ahead in SD (66 vs 24 avg), MN (88 vs 47 avg) and MI (61 vs 24 avg).

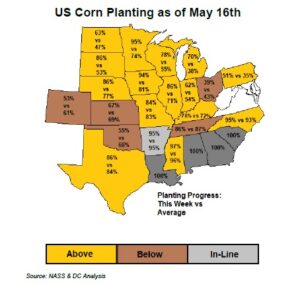

Corn futures managed small gains. Market may have corrected an overbought tech picture. CN chart formation could be negative if we do not trade over 6.84. First resistance in 6.73. Corn futures rallied after USDA announced another 1.36 mmt US 2021/22 new crop corn sold to China. This suggest sales near 8 mmt. They may have bought 10-12 mmt to date. Corn also supported by talk that China could take all US old crop open unshipped sales. This could push their total imports to over 30 mmt versus USDA 26. Some feel Brazil 2021 corn crop will be below 90 mmt. USDA estimates Brazil corn exports near 34 mmt. Shipments to date are near 18 mmt. July-Sep needs to be near 16 mmt to reach USDA goal. There previous record July-Sep exports were 13 mmt. Some feel they may export only 10 mmt which would reduce their export by 325 mil bu, Still, if US 2021 corn acres are near 96 and a 180 yield, increase export demand would be offset by higher supply. US corn planting was reported at 80 pct vs 68 average. Corn planting was most behind in CO (53 vs 61 avg) and OH (39 vs 43 avg). Corn planting was most ahead in SD (86 vs 53 avg), MI (70 vs 38 avg), and WI (78 vs 55 avg).

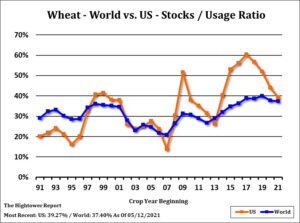

Choppy wheat trade. WN settled near 6.98. Range was 6.92-7.18. Favorable US SRW crop conditions, slow export interest and weak tech picture offset a lower US Dollar. KWN settled near 6.48. Range was 6.42-6.70. Annual KS crop tour estimate of the KS crop could weigh in prices. USDA estimated US winter wheat HRW ratings were mixed this week with TX rating dropped by 5 pct to 25 G/E, OK rating held steady at 59 pct G/E. KS rating improved 1 pct to 54 G/E. Spring wheat planting at 85 pct versus 71 average. Dry topsoil moisture is allowing a rapid planting pace. China April wheat imports were near 900 mt. Season to date imports 3.8 mmt and up 147 pct yoy. USDA estimated World 2021/22 wheat crop near 789 mmt vs 776 this year. Domestic feed is 158 mmt vs 157 this year. Trade near a record 202 mmt vs 199 this year. End stocks 295 mmt vs 294. Russia crop est near 85 mmt vs 85 this year. Exports 40 mmt vs 39 this year.