Written Commentary

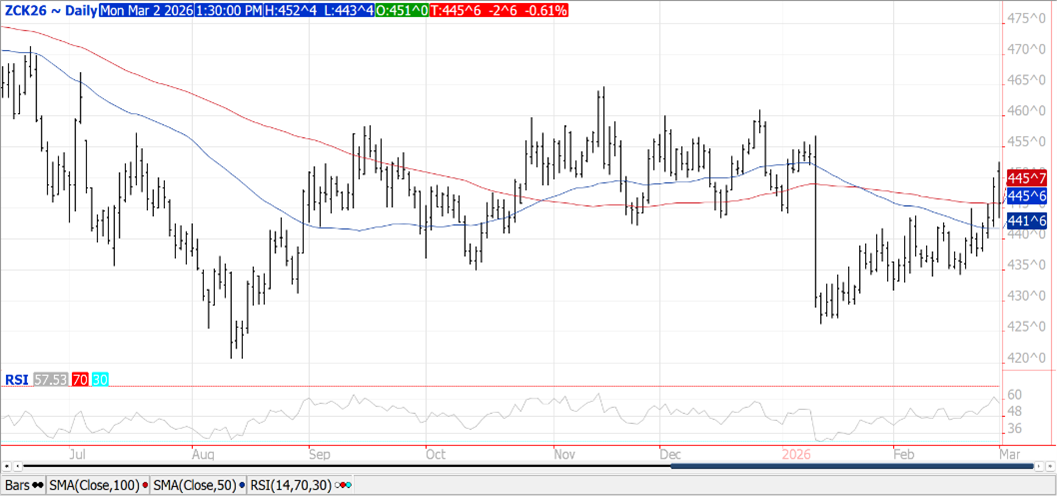

Prices ranged from slightly higher for new crop futures to $.05 ½ lower for old crop. May-26 was down $.02 ¾ rejecting trade above $4.50 and a 7 week high overnight. Deliveries against the Mch-26 contracts surged to 448 contracts, up from only 9. AgRural reports 2nd corn plantings across Brazil have reached 66%, up from 50% the previous week. Safras & Mercado lowered their Brazilian production forecast 1.2 mmt to 141.7 mmt, still well above the USDA est. of 131 mmt. Export inspections at 73 mil. bu. were above expectations and above the 64 mil. bu. needed per week to reach the USDA forecast. YTD inspections at 1.560 bil. are up 45% from YA vs. the USDA forecast of up 16%. Noted buyers were Mexico – 20 mil. and Korea – 11 mil. The Ave. price for Dec-26 corn in February set the spring based insurance revenue guarantees at $4.61 ½, just below the last 2 years and the lowest since 2021. Corn used for the production of ethanol in Jan-26 at only 461 mil. bu. was well below expectations of 483 mil. In addition usage in Dec-25 was revised lower by nearly 6 mil. bu. to 483. Today’s data would suggest sorghum usage as a feedstock continues to grow. In the first 5 months of the 25/26 total corn usage has reached 2.318 bil. bu. down .5% from YA vs. the USDA forecast of up 3%. The USDA corn usage est. is starting to look too high.

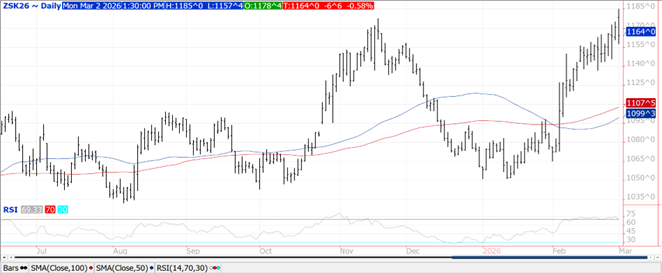

Prices were mixed closing well off session highs. Soybean prices ranged from down $.04-$.07 for old crop futures while up less than $.01 on new crop. Meal was $4-$8 lower while oil was up 80-90 points. May-26 beans traded to its highest level in nearly 2 years at $11.85 before turning lower. May-26 meal held support above its 100 day MA at $310.60. New contract high for May-26 oil while the spot contract traded to a 2 ½ year high. Surging energy prices triggered by the US/Israeli attack on Iran fueled another wave higher in soybean oil prices. Other areas of the Ag. space turned lower as China formally denounced the US military action which could jeopardize the Trump/Xi meeting later this month. Spot crush margins rebounded another $.01 to $2.12 bu. while bean oil PV improved to just over 50%. AgRural lowered their Brazilian production forecast 3 mmt to 178 mmt, just below the USDA est. of 180 mmt. Brazilian harvest has reached 39%. Bean oil usage for biofuel production in Dec-26 at only 859 mil. lbs. was the lowest since April-25. In the first 3 months of the 25/26 MY usage at only 2.795 bil. lbs. is off 22% from YA, vs. the USDA forecast of up 26%. The USDA will need to shift usage for 25/26 away from biofuels. MM’s bought just over 75k contracts across the soybean complex extending their combined long position to nearly 280k contracts, just shy of the Nov-25 high. Export inspections at 42 mil. bu. were above expectations. YTD inspections at 962 mil. are down 30% from YA vs. the USDA forecast of down 16%. China took 27 mil. while Germany took 5 mil. and Mexico 4 mil. Crush in Jan-26 at 227.8 mil. bu. was slightly above expectations. YTD usage at 1.119 bil. bu. is up 7.4% from YA vs. the USDA forecast of up 5.1%. Crush Feb-26 thru Aug-26 will need to reach 1.451 bil. bu. vs. 1.402 bil. YA. Bean oil stocks rose 11.7% to 2.433 bil. lbs., slightly above expectations and the highest since April-23. With the recent surge in crush margins I’d expect the USDA to raise their forecast 10-20 mil. bu. in next week’s WASDE.

Prices ranged from $.03 lower in MIAX to $.14 lower in CGO. CGO May-26 rejected trade above $6.00 for the first time since July-25. KC May-26 also stretched out to its highest level since July-25 before backing up. MM’s bought a record amount of CGO wheat in the week ended Feb. 24th at nearly 51k contracts, however were still net short 17k. MM’s bought nearly 15k contracts of KC futures flipping their net position to net long for the first time since Aug-23. Saudi Arabia bought nearly 800k mt of wheat for May/June shipment. Prices reportedly ranged from $265.60-$283/mt CF, while likely sourced from Russia or other Black Sea origins. Export inspections at 13 mil. bu. were at the low end of expectations and below the 16 mil. bu. needed per week to reach the USDA forecast. YTD inspections at 684 mil. bu. are up 19% from YA, vs. the USDA at up 9%.

Charts provided by CQG

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.