Written Commentary

SOYBEANS

This morning’s EU weather models added rain back into the forecast for Central Argentina over the weekend and early next week. Accumulations of .50” – 1.50” are expected for Cordoba into northern Buenos Aires. Beyond early next week hot/dry conditions are set up for the next week to 10 days. The midday GFS model was not near as generous with beneficial moisture. Jan-23 soybeans came within ½ cent of this week’s high of $15.16 ¾ before backing off. Jan-23 soybeans finished at $15.08 ¾ up $.02 ¼. After trading both sides of unchanged soybean meal is closed $2 – $3 lower. Jan-23 soybean oil closed at 66.40 up .60, just below its 100 day MA at 66.56. In yesterday’s tender Egypt reportedly bought 42k mt of vegetable oil, 30k soybean oil at $1,415/mt and 12k of sunflower oil at $1,330. Argentine farmers have sold 79% of their 2021/22 soybean crop slightly below YA despite the preferential currency program. This currency program ends this week. Tomorrow’s export sales report is expecting soybean sales 30 – 36 mil., soybean meal 100 – 325k tons, and soybean oil 0 – 5k tons.

CORN

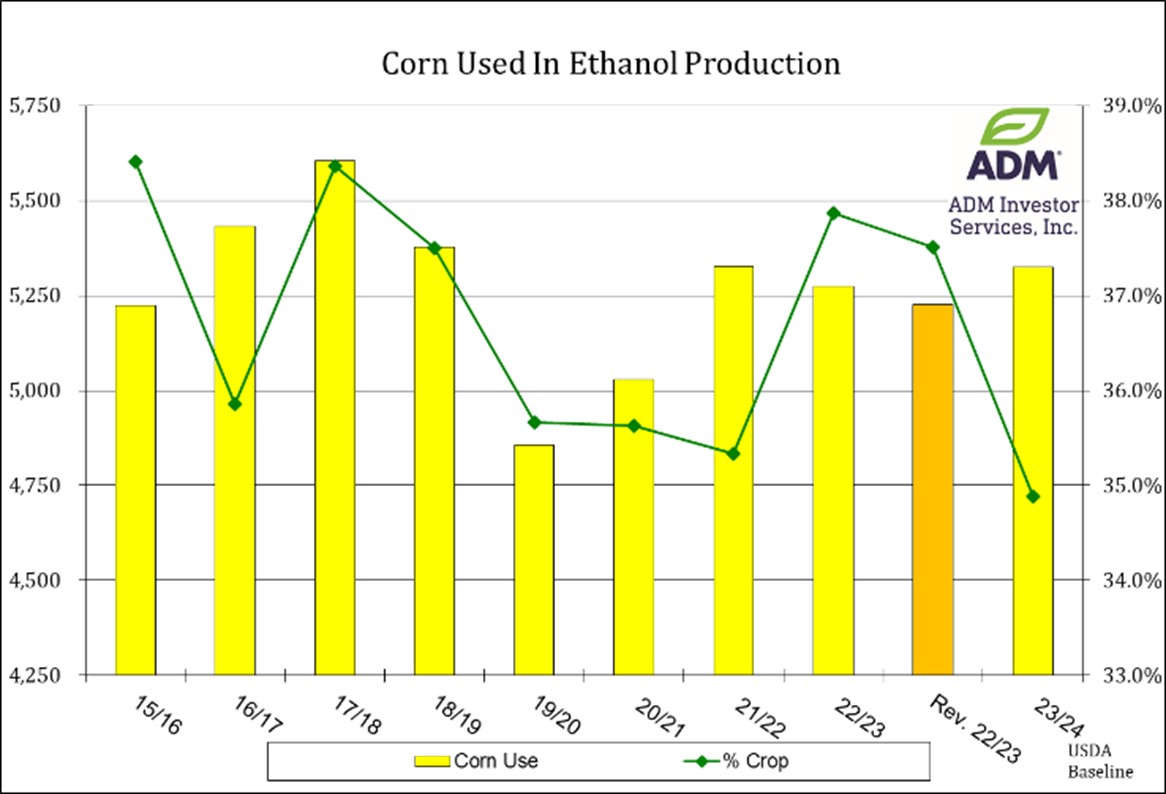

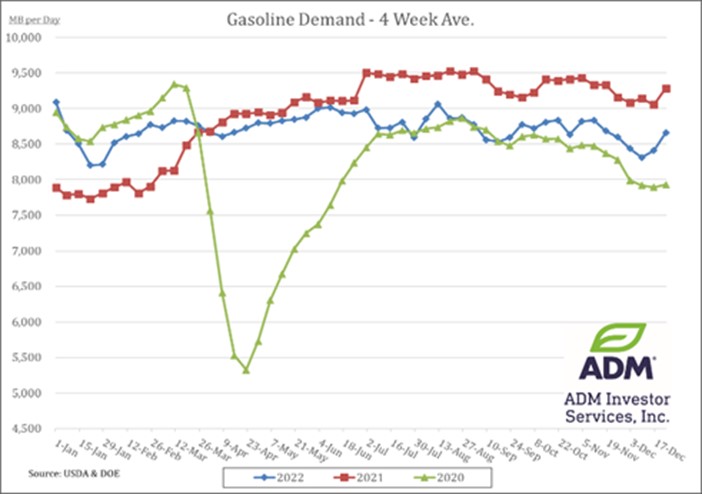

Prices closed with moderate losses giving back roughly half of yesterday’s gains. Mch-23 closed at $6.79 ½. The 100 day MA now serves at the first support level at $6.70 ½. Argentine farmers have sold 74% of last year’s corn crop, down slightly from 77% from the previous year. Ukraine grain shipments did improve last week with roughly 1.2 mil. tons. of corn leaving Black Sea ports as of Dec. 25th, more than double the 514k from the previous week. Ethanol production last week at 963 tbd was below expectations and down 9% from this week YA. Corn usage at 96 mil. bu. was below the pace needed to reach the USDA forecast. Despite the lower than expectation production, stocks rose to an 8 month high of 24.6 mb, up from 24.1 mb the previous week and well above the 20.7 mb from YA. While overall US gasoline consumption spiked last week, typical for the Christmas Holiday, it was still down 9% from YA. US gasoline demand has been below YA levels for 13 consecutive weeks. Given the weak demand for fuel along with recessionary fears for 2023 I’m leaning toward a 50 mil. bu. reduction to the current USDA usage forecast of 5.275 bil. Tomorrow’s export report expected to show corn sales 25 – 35 mil. bu.

WHEAT

Wheat prices fell sharply on the open having traded $.20 lower in all 3 classes. Heavy rains are forecast for very eastern Texas and along the entire gulf coast pushing into the southern Midwest over the next 5 days. Still little moisture for the drought stricken southern plains. 69% of the US winter wheat crop is in a drought, up 2% from last week. US spring wheat area was unchanged with 69% impacted by drought. Despite continued missile strikes by Russia, Ukraine grain keeps flowing from the Black Sea. Russian crop estimates and export forecasts continue to grow as they continue to undercut all foreign competition.

See more market commentary here.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.