Written Commentary

SOYBEANS

Soybeans found support on talk of firmer US domestic basis and talk that China hog margins were moving higher and could suggest that China could begin to buy US soybeans. Trade estimates US soybean export sales near -100/300 mt old crop and 300-650 mt vs -66 and 477 last week. Last week, US total commit was 59.5 mmt vs 61.9 ly. USDA goal is 58.8 mmt vs 61.6 ly USDA est World soybean trade near 153.1 vs 164.6 ly. Brazil is 80.0 vs 94.8 last year. USDA est World 2022/23 soybean exports at 169.1, with Brazil 89.0 and US 58.6. Noon GFS weather maps reduce some rains early next week from OH to SC and may have added too much rain from N Plains through MN and NE. Tropical cyclone could move into Florida and Alabama Coast Aug 28. Some feel SX in 13.50-14.50 range into US harvest.

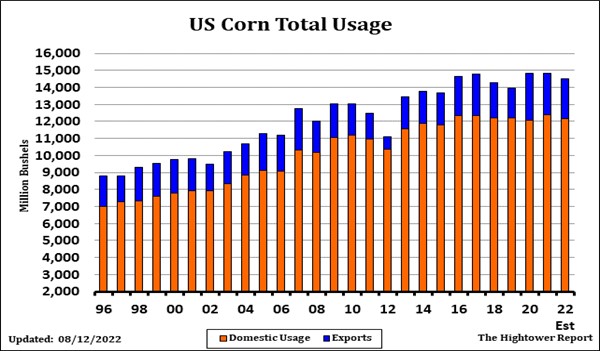

CORN

Corn futures ended slightly higher with CZ in a 6.06-6.14 range. Some feel CZ could be in a 5.80-6.40 range into US harvest. US corn basis is lower due to increase SW harvest but some feel lower crops there could eventually push prices higher. Some estimate US SW states total feedgrain supply could be down 500 mil bu due to dry weather. Brazil corn export prices are below US but US is competitive November forward. Talk of increase Ukraine exports offers resistance. Key could be where EU buys their import corn. Weekly US ethanol production was down 4 pct from last week and up 1 pct vs ly. Stocks were up 1 pct from last week and up 9 pct from last year. Margins remain negative. Weekly US corn exports sales are est near 0-300 mt old crop and 100-600 mt new vs 192 and 191 last week. There were reports that Ukraine has 5 ships arriving at Chornomorsk port to load 70 mt of grain. This is largest convoy since UN deal. USDA est World corn trade near 200.4 mmt vs 182.6 ly. US 62.2 vs 69.8, Brazil 44.5 vs 40.9, Argentina 39.0 vs 40.9 and Ukraine 24.5 vs 23.8 ly. USDA est World 2022/23 corn trade at 185.6 with US 60.3, Brazil 47.0, Argentina 41.0 and Ukraine 12.5.

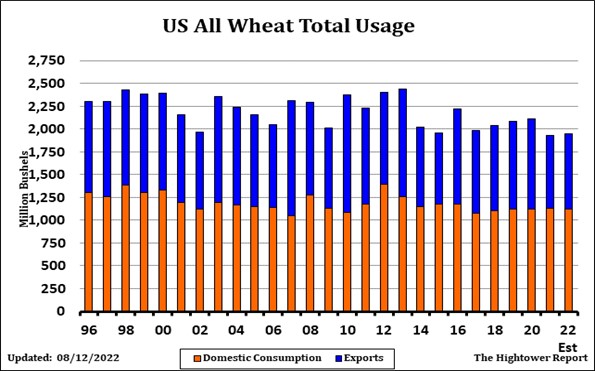

WHEAT

Wheat futures were lower initially on talk of higher Russia exports, increase Ukraine exports, concern that higher inflation could lower global food demand, lower equity markets and higher US Dollar. Rains in the US south plains also offers resistance to wheat futures. Russia attacks on city of Odessa raises concern about Ukraine export pace. US and World end users are uncovered for 2023 which could eventually offer support. Word that Iraq may have passed on a tender for US wheat due to too high prices may have also weighed on wheat futures. Weekly US wheat export sales are est near 200-600 mt vs 359 last week. USDA est World wheat trade at 208.6 mmt vs 201.8 ly. Russia 42.0, EU 33.5, Canada 26.0, Australia 25.0, US 22.4, Argentina 13.0 and Ukraine 11.0. Last year, Russia was 33.0, EU 31.7, Canada 15.0, Australia 27.5, US 21.7, Argentina 16.6 and Ukraine 18.8. Key could be actual Russia and EU exports.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.