Written Commentary

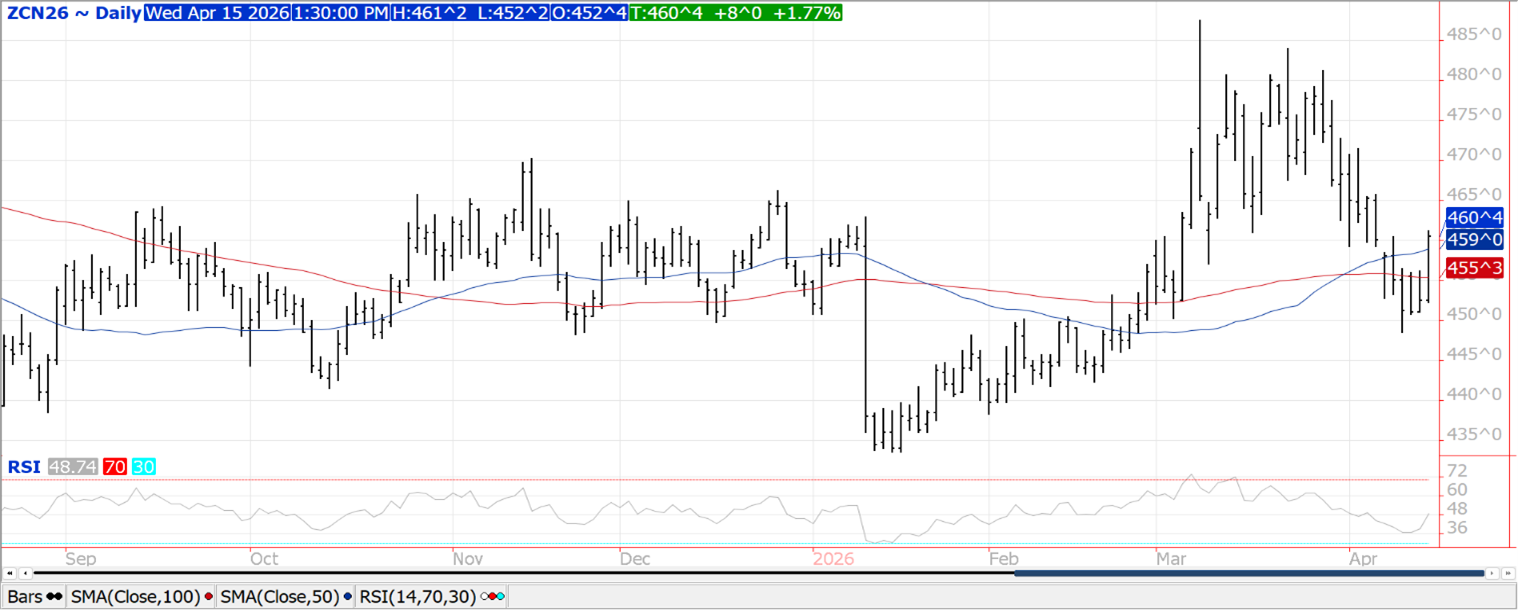

Prices were $.08 higher finishing near session highs while spreads were mixed. July-26 recently rejected trade below $4.50 while today closing above its 50-day MA. Despite the big discrepancy between the USDA and SA production forecasts, US FOB offers remain competitive into the summer months. Expectations for tomorrow’s export sales are 32-70 mil. bu. Plantings in the SE half of the Midwest are moving along at a rapid pace while not at all in the soaked N. Midwest. Ethanol production rose to 1,120 tbd, or 329 mil. gallons in the week ended April 10th, up from 328 mil. the previous week and 10.7% above YA. Production was above expectations. There was 110 mil. bu. used in the production process, or 15.78 mil. bu. per day, above the 15.4 pace needed to reach the USDA forecast of 5.60 bil. bu. In the MY to date there has been 3.40 bil. bu. used, or 15.3 mbd, an annualized pace of 5.590 bil. Ethanol stocks jumped to 26.7 mil. barrels, above expectations while matching YA.

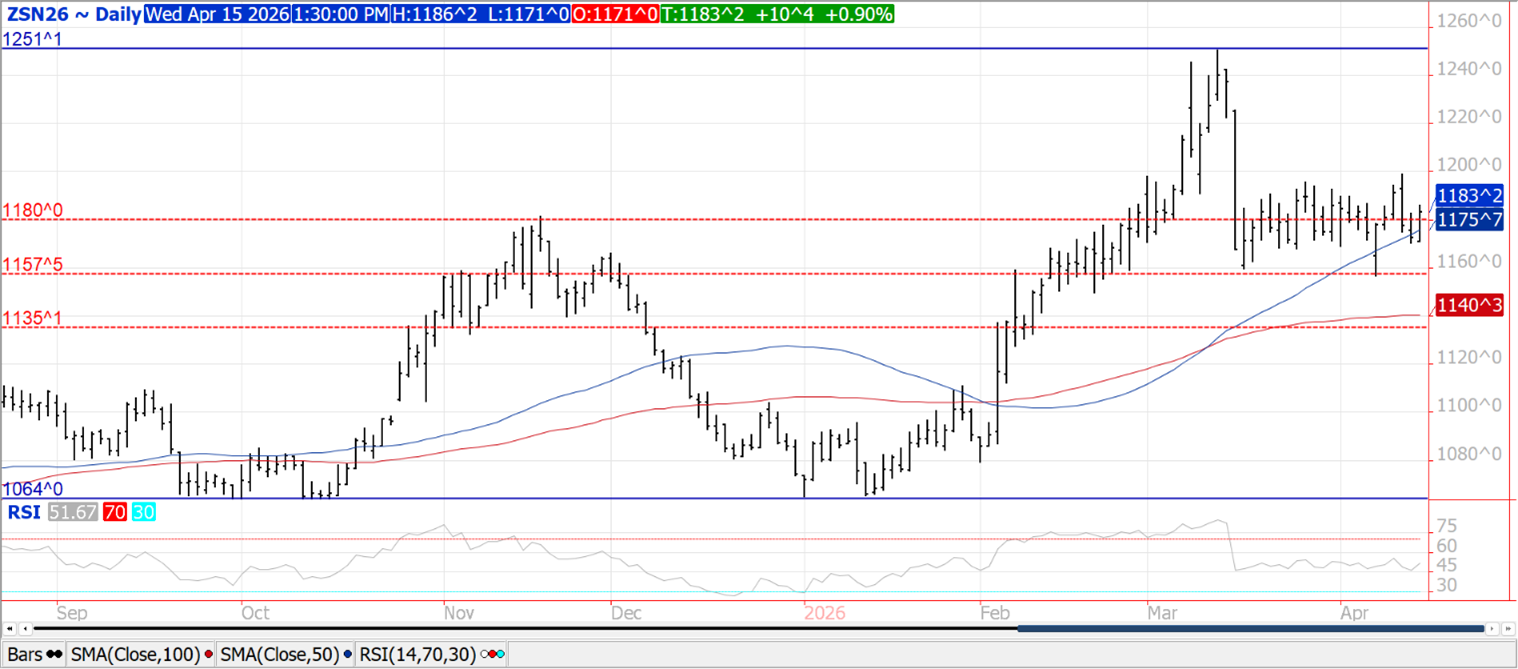

Prices were moderately higher across the complex with beans up $.09-$.11, meal was $2-$5 higher while oil was up over $.01 lb. Spreads were mixed in soybeans while firmer in the products. Spot crush margins surged another $.14 to $3.12 bu., a fresh 3 ½ year high, while bean oil PV improved to 50.3%. NOPA crush at 226 mil. bu. was below the Ave. estimate of 230 mil. however, within the range of est. Processing was well above the 209 mil. bu. in Feb-26 and the 194.5 in Mch-25 however failed to reach the all-time high of 227.65 in Oct-25. Implied census crush at 231 mil. bu. would bring YTD to total to 1.565 bil. bu., up 9% from YA vs. the revised USDA forecast of up 7%. To reach the current USDA est. of 2.610 bil. bu. crush over the last 5 months of the MY will need to reach 207 mil. bu., up 4% from YA. Bean oil stocks at only 2.04 bil. lbs. were below expectations of 2.173 while falling from 208.8 the previous month. Tomorrow’s export sales are expected to range from 8-22 mil. bu. of soybeans, 300-600k tons of meal and -10 – 14k tons of oil.

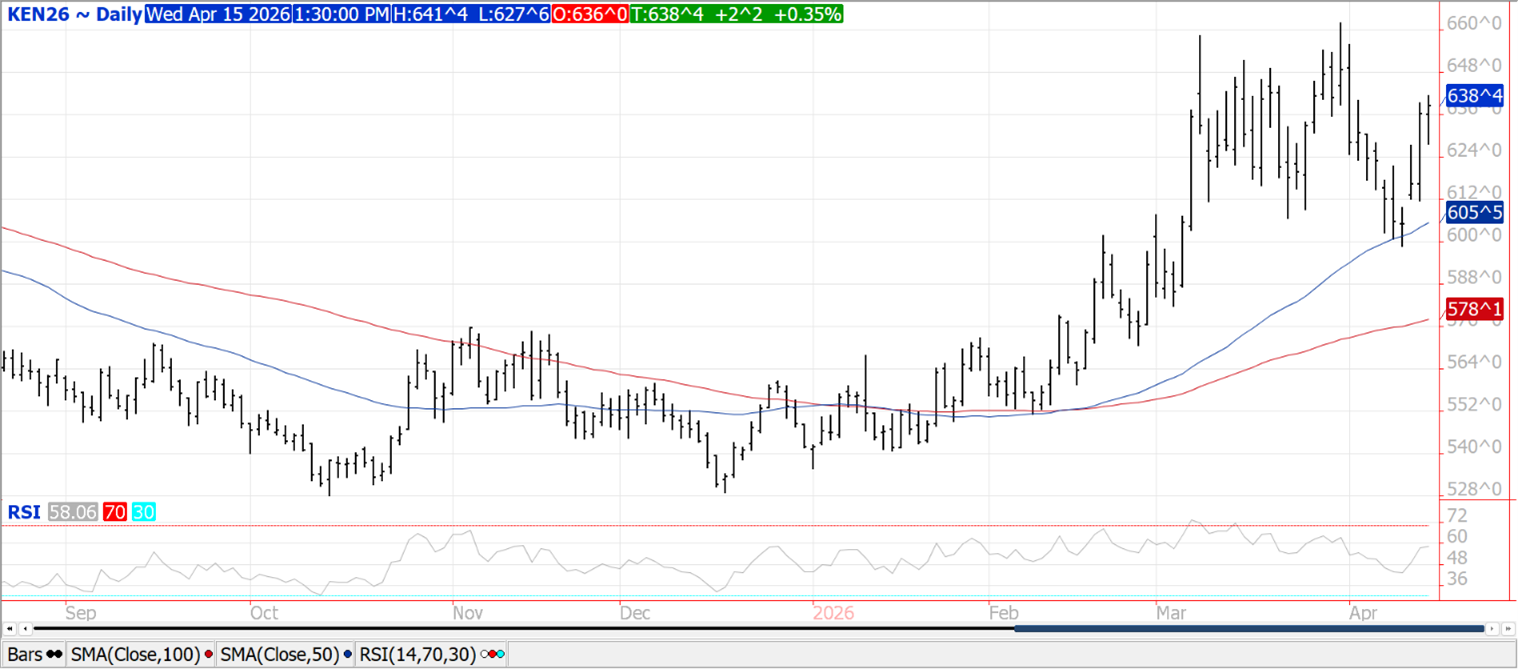

Prices recovered late closing $.01-$.03 higher across the 3 classes. Spreads were mixed. CGO July-26 managed to close back above $6.00 for a 2nd consecutive session. KC July-26 has resistance at last month’s high of $6.62 ¼. World Weather doesn’t expect freezing temperatures late this week to be low enough for long enough to seriously impact the HRW crop. Drought conditions in the far Western plains continue to deepen however as rains have stayed east. EU soft wheat exports as of April 12th at 18.57 mmt are up 8% YOY. Awaiting results of Algeria’s 50k mt tender for durum wheat. Export sales are expected to range from 6-18 mil. bu.

Charts provided by CQG

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.