>>Read the complete, in-depth June 2026 Edition HERE

KEY HIGHLIGHTS

CORN

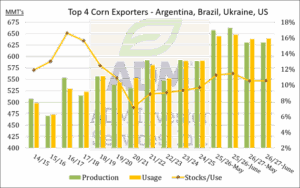

USDA June WASDE saw US 2025/26 corn ending stocks increased by 3 million bushels to 2.145 billion, slightly above expectations.

Exports were increased by 25 million bushels, with usage for ethanol down 25 million and imports up 3 million.

2025/26 global ending stocks jumped by 6.4 million metric tons to 303.4 million.

2025/26 Argentina’s production was revised up by 2 million metric tons to 61 million, Brazil’s was up 3 million tons to 138 million, and India’s up 8.9 million.

US 2026 corn production was left unchanged at 15.995 billion bushels, in line with expectations.

SOYBEANS

US 2025/26 ending stocks were left unchanged at 340 million bushels in the USDA’s June WASDE report.

Exports were down 20 million bushels, offset by a 20 million-bushel increase in crush.

Soybean oil usage for biofuels was revised up by 350 million pounds to 14.55 billion, absorbing higher supplies.

Meal exports and domestic usage were up 450,000 tons

Argentine production was up 2 million metric tons to 50 million, mostly offset by higher usage.

WHEAT

The June WASDE report left US 2025/26 wheat ending stocks unchanged at 935 million bushels.

Global stocks were revised up by 800,000 metric tons to 279.95 million.

2026 US all-wheat production was revised down 18 million bushels to 1.543 billion, 12 million below expectations.

Winter wheat production was down 18 million bushels to 1.030 billion.

Average winter wheat yield was estimated at 46.8 bushels per acre, the lowest in more than a decade.

COCOA

Ivory Coast port arrivals for the week ending June 14 were estimated at 32,000 metric tons, up from 17,000 for the same week last year. Cumulative arrivals for the 2025/26 marketing year have reached 1.854 million tons, up from 1.575 million last year and the highest for this point in the season since 2022/23. The five-year average is 1.861 million.

Data from Ivory Coast exporters’ association GEPEX put the nation’s May cocoa grind at 55.769 metric tons, up 39.7% from the year earlier. Cumulative grind since the marketing year began in October reached 437,118 tons by the end of May, up 1.7% from the same period last season.

COFFEE

Unseasonable rains in Brazil are slowing the harvest, interrupting drying, and raising concerns about the potential for bacterial and fungal diseases.

Reuters reported that most coffee-producing areas in southeast Brazil, including the main producing state of Minas Gerais, had three consecutive days of rain from June 11 to June 13 during what is typically the dry season. One farmer told Reuters that at least 10% of his berries must have dropped from trees. The excess rainfall being blamed on El Nino, and meteorological data from LSEG shows precipitation may exceed historical averages between during the second half of June.

COTTON

The trade seems to be encouraged by demand prospects while remaining concerned about the lack of moisture in west Texas.

World Weather Inc. was expecting an erratic distribution of rain in west Texas for the latter part of June, with very few areas getting enough rain to seriously counter evaporation.

SUGAR

The peace deal between the US and Iran upsets one of the key supportive factors for sugar recently – the idea that high oil prices will encourage more use of cane for ethanol instead of sugar production.

There is the potential that the reopening of the strait will support demand for raw sugar from refineries in the Persian Gulf that have been locked in since the strait was closed, but that does not ease concerns about excess supply.

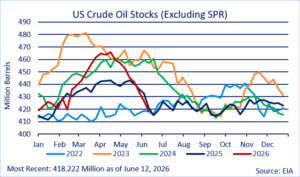

CRUDE OIL

August Crude Oil gapped lower on the news that the US and Iran had agreed to a memorandum of understanding that would include a 60-day cease fire, a reopening of the Strait of Hormuz within 30 days, and an end to the US blockade of Iranian ships. The issues of Iran’s nuclear program and other thorny points still have to be resolved. Officials said both sides would hold detailed discussions on these over the next 60 days.

Industry experts point out that it will take weeks to months to get oil flows back to normal, but this is to be the most positive news since the war began, and it makes the drawdowns of reserve stocks look less dire.

NATURAL GAS

The potential restoration of LNG flows through the Strait of Hormuz means that US exports could start to see competition from Qatar, but it could take also quite a while for that country to see its flows return to where they were prior to the war after the damage their plants suffered from Iranian attacks. At the time of the attacks, there were estimates that it could take years to recover.

The weather forecast as of mid-June showed a mix of temperatures across the lower 48 states that did not suggest a surge in cooling demand. The 6-10-day forecast had below normal temperature from the Midwest to the east coast and above normal out west and in the south.

LIVE CATTLE

US beef imports have been increasing this year; as of the second week of June, 2026 imports were up 11% from a year prior.

The imports consist mainly of lean beef trimmings and low grade beef which are used primarily for fast food restaurants.

US imports have averaged about 2,025 loads per week on load weights of 40,000 pounds.

LEAN HOGS

As of June 15 federal hog slaughter was down 342,441 head (-0.5%) from the same period in 2025, but due to heavier hogs weights, US pork production was up 0.3%.

Pork prices have slowly dropped. Between May 1 and June 15, the CME Pork Carcass Index fell from from $97.79/cwt to $96.23.

Lean Hog futures no longer have contracts trading above $100. June Lean Hogs expired at $92.52.

STOCK INDEX FUTURES

Stock index futures have consolidated choppy, two-way price action over the past month, after the powerful April–May rally ran out of momentum. The S&P 500 spent much of late May grinding higher, until elevated Treasury yields and geopolitical risk sparked a tech pullback in early June. It was not until optimism around a US-Iran peace deal in the second week of June that the equities began reversing earlier losses. The US-Iran war and its seeming resolution have shaped virtually every asset class since its announcement.

The macro narrative continued to dominate price action. The May CPI showed headline inflation accelerating to 4.2% YoY, while core CPI ticked up to 2.9% from 2.8% and shelter posted a 3.4% gain. The PPI report showed final demand prices rising 1.1% MoM and 6.5% YoY, the largest 12-month rise since November 2022. Both readings reflected the surge in energy prices rather than a broad rise in prices across the economy.

CURRENCIES

The US dollar was rangebound over the past month. The May CPI and PPI releases alongside May’s hiring figures reinforced the narrative that US Fed policy is set to remain on hold, with money markets are modestly biased toward one hike in late 2026.

The 2-Year Treasury yield rose well above the upper bound of the Fed Funds rate to over 4%. Several board members at the Fed are keeping the door open to rate hikes, which has underpinned the dollar.

INTEREST RATES

Treasury yields have been at the mercy of the oil market ever since the conflict in Iran began. The 2-Year Note remaining above 4% is the strongest signal that the bond market is not completely assuaged by recent news of a US-Iran peace, nor by the following drop in oil prices, broadly signaling that policy could move upwards. Recent inflation data reinforced a hawkish-leaning hold, but it did counter any immediate urgency to move rates higher. May’s nonfarm payrolls data have likely provided the Fed with enough support to raise rates without worrying over consequences to the labor market – if they choose to do so.

Underlying inflation fundamentals are structurally bearish for bonds in the near-term, especially as expectations of a hike in policy from the Fed grow. The obvious downside risk for yields is how quickly inflation falls following a reduction in oil prices. If inflation fails to decline, then expectations of a Fed hike are likely to grow.

GOLD & SILVER

Gold has trended downwards since mid-May as it has navigated a challenging macroeconomic environment in which higher Treasury yields, a stronger dollar, and a hawkish repricing of Fed rate expectations have weighed on prices.

The core challenge for gold is the same one that pressured prices in recent months, and it has intensified. With May CPI reaching 4.2% YoY and core CPI at 2.9%, headline inflation is running over double the Fed’s 2% target.

COPPER

COMEX copper futures have largely moved higher since mid-May, hitting a local high of $6.65 before slipping towards $6.30.

Supply worries continue in the global market following the incident at Freeport McMoran’s Grasberg mine in Indonesia, the world’s second largest, which will cause further production delays.

Interested in more futures market commentary? Explore our Market Dashboards here.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.