Written Commentary

Trade tariff tensions aside, though clearly still front and centre, while there are items of interest in the modest data schedule via way of UK BRC Retail Sales, French Unemployment (both better than expected) and the US NFIB Small Business Optimism, it will be Powell’s testimony, a speech by BoE hawk turned uber dove Mann (though pre-mpted by her interview in the FT today)), an array of commodities events, and corporate earnings from SMIC, BP, Coca Cola, DuPont and Globalfoundries which attract more attention. In commodities and energy, the focus will be on the EIA’s monthly Oil Market and the USDA’s WASDE reports, with the India Energy Week and Oslo Energy Forum also getting under way. Of particular interest will be the EIA assessment of US 2025 oil output, given that the rapid expansion of recent years looks set to slow sharply, and with inventories at low levels and tighter curbs of Russian exports, this should impart some support for crude prices, despite tepid demand growth prospects. To be sure there remains a lot of mothballed OPEC output, but OPEC+ looks unlikely to open the output taps and may even extend the delay to its previously announced output expansion, absenting a much sharper and sustained rise in prices. The USDA’s WASDE is not expected to see any dramatic S&D changes, and comes against the backdrop of concerns about the potential impact of Trump’s ‘reciprocal tariffs’, and a further weather related deterioration of Russian wheat exports. Now that the US has imposed 25% steel and aluminium import tariffs. The key question is how other countries respond as a gauge of the escalation threat.

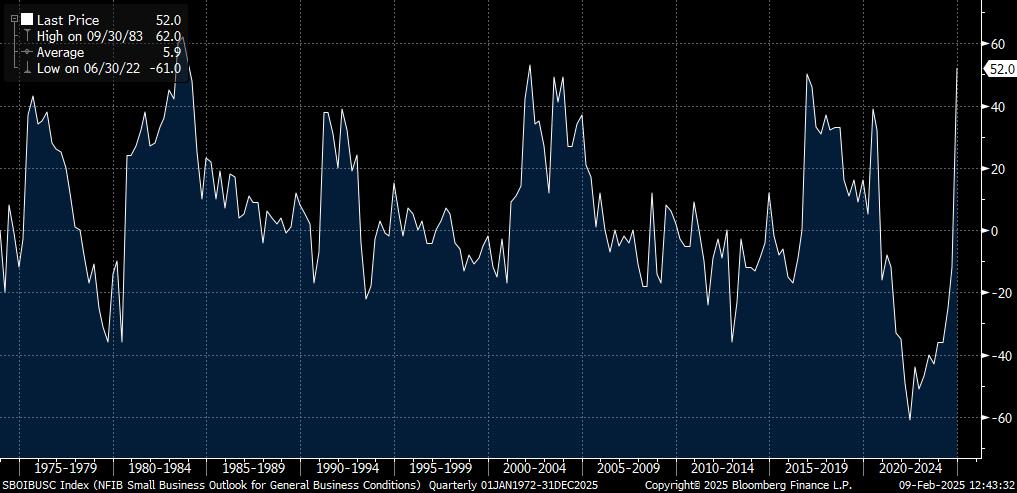

** U.S.A. – Powell testimony, Jan NFIB Small Business Optimism **

– Ahead of tomorrow’s CPI, the focus is on Powell’s semi-annual testimony. Powell will doubtless face a lot of tough questions, but if the already published written report is a guide, which has almost no mentions of the potential impact of trade tariffs or other government measures on growth, inflation or the labour markets, then he will stick to the line that the Fed will not ‘speculate’ about the impact, and wait to see what tariffs and other measures are delivered. By extension, the implication is that the Fed’s rate pause is likely to be protracted, even if some FOMC officials will doubtless expound on the potential impact in speeches. NFIB Small Business Optimism (median forecast 104.7 vs. prior 6 year high of 105.1) will bear some scrutiny, given that the recent surge has been above all powered by the ‘Expect Better Economy’ sub-index, which has seen a record surge since September (see chart), which may falter on the back of tariffs, though this may not show up until February’s survey.