Written Commentary

Overnight trade has SRW Wheat up roughly 8 cents; HRW up 10; HRS Wheat up 8, Corn is up 8 cents; Soybeans up 22 to 15 cents; Soymeal up $4.00, and Soyoil up 135 to 75 points.

Chinese Ag futures (September) settled up 63 yuan in soybeans, up 43 in Corn, up 147 in Soymeal, up 144 in Soyoil, and up 184 in Palm Oil.

Malaysian palm oil prices were up 57 ringgit at 3,951 (basis July) at midsession on tight production, soyoil gains.

U.S. Weather Forecast: Last evening’s GFS model run was notably wetter in the Northern Plains in week 2 of the outlook compared to the midday GFS model. This is evidence of a potentially more active pattern in the Northern Plains and in the southern Canada Prairies. Rain prospects are still expected to improve in early May for both of these regions which will be beneficial for increasing soil moisture.

South America Weather Forecast: The lack of much change in last evening’s GFS model run again keeps confidence high in the forecast. Some shower and thunderstorm activity will still be locally meaningful from Rio Grande do Sul into Parana, Brazil Friday through Sunday; though, this rain is unlikely to reach Sao Paulo, western Minas Gerais, eastern Mato Grosso do Sul, and southern Goias. This will keep concerns elevated about production in this area during May due to monsoonal rainfall ending in much of Brazil over the next couple of weeks.

Conditions in Argentina will still be mostly good; though, rain in the region through Saturday will lead to some fieldwork delays and may slow crop maturation.

The player sheet had funds net buyers of 9,000 contracts of SRW Wheat; net bought 27,000 contracts of Corn; net bought 12,000 Soybeans; bought 1,000 Soymeal, and; net bought 8,000 Soyoil.

We estimate Managed Money net long 16,000 contracts of SRW Wheat; net long 488,000 Corn; net long 196,000 Soybeans; long 56,000t Soymeal, and; net long 111,000 Soyoil.

Preliminary Open Interest saw SRW Wheat futures up roughly 450 contracts; HRW Wheat down 990; Corn up 15,100; Soybeans up 960 contracts; Soymeal down 460 lots, and; Soyoil up 1,600.

There were no changes in registrations—Registrations total 10 contracts for SRW Wheat; ZERO Oats; Corn ZERO; Soybeans 5; Soyoil 968 lots; Soymeal 175; Rice 1,013; HRW Wheat 1,291, and; HRS 235.

Tender Activity—Japan bought 85,110t U.S./Canadian wheat—

For the week ended Apr 16th, ethanol production was 941,000 barrels per day, unchanged versus a week ago, up 67.0% versus a year ago.

Stocks were 20.4 mil barrels, down 0.4% versus last week, down 26.2% versus last year.

Corn used was 95.1 mil bu versus 95.1 mil last week and versus the 97.3 mil needed to meet USDA projections.

Worsening conditions in Southwest U.S./Southern Plains lower U.S. winter wheat yield – Refinitiv Commodities Research

—2021/22 U.S. WHEAT PRODUCTION: 48.7 [44.3–52.5] MILLION TONS, DOWN 1% FROM LAST UPDATE

—Updated weather and condition scores lower 2021/22 U.S. wheat production 1% to 48.7 [44.3–52.5] million tons. Our current median estimate puts national-level winter wheat yield at 50.0 bushels per acre (bpa), with a range from 46.3 to 52.6 bpa, 1.4% below trend yield of 50.7 bpa. This leads to total winter wheat production of 33.9 [31.3–35.6] million tons, down 1.3% from last update.

—Spring wheat production is unchanged at 14.8 [12.9–16.9] million tons (with durum and other spring wheat at 1.4 and 13.4 million tons, respectively).

Chinese buyers are thought to have booked at least half a million tonnes of new-crop French wheat for shipment between July and September, suggesting China will remain a major outlet for French exporters. Some sources estimated the volume at 500,000 to 600,000 tonnes, or up to around 10 large panamax vessels, mainly for August. Others pegged total sales higher, at around 1 million tonnes, suggesting France could load up to about 15 panamaxes this summer.

A report issued by the U.S. Department of Agriculture’s Foreign Agricultural Service post in Beijing estimated China’s corn imports for the 2020/21 marketing year at 28 million tonnes, above the USDA’s official estimate of 24 million. The report, dated April 16 and posted online on Wednesday, attributed the increase to “continued feed demand and a supply deficit that supports restocking of reserves.”

—The report also projected China’s 2021/22 corn imports at 15 million tonnes.

High prices and increased sown area set China corn production outlook at 267 mmt – Refinitiv Commodities Research

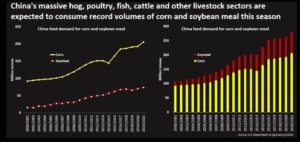

China issued guidelines on Wednesday recommending the reduction of corn and soymeal in pig and poultry feed, a measure that could reshape the flow of grains into the world’s top corn and soybean buyer.

China’s top pig producers are set to report a plunge in first-quarter profits from the huge gains of last year, after hog prices fell, and disease, more expensive feed and poorly performing sows further eroded earnings. The earnings declines began in the fourth quarter of 2020 and margins are still under pressure, said analysts, as companies face ongoing challenges and costs in recovering from African swine fever, which ravaged the country’s hog herd in 2018 and 2019 and saw a resurgence this winter. Hog prices fell 40% in the first quarter as farmers rushed to liquidate herds amid a wave of spreading disease and as pork demand during the Lunar New Year disappointed.

Argentine farmers are expected to plant 6.5 million hectares with 2021/22 wheat, unchanged from the previous season, the Buenos Aires Grains Exchange said in a report. Argentine wheat sowing starts in May. Harvesting ends in January. Good international grain prices “support a planting intention similar to that of last year. That is to say: an area of 6.5 million hectares,” the exchange said in its first wheat forecast of the season.

Argentine farmers have sold 14.37 million tonnes of 2020/21 soybeans, a figure that lags last year’s sales tempo, the Agriculture Ministry said on Wednesday in a report with data updated through April 14. Bad weather recently prompted the Buenos Aires Grains Exchange to cut its 2020/21 crop estimate to 43 million tonnes from a previous forecast of 45 million tonnes. Harvesting on the Pampas grains belt started earlier this month. The ministry said the pace of sales is lagging last year, when growers had sold 19.23 million tonnes of soybeans by the same date. Farmers have been reluctant to sell this year amid uncertainty about the foreign exchange rate.

Russian wheat exporters are bidding aggressively for new business, even though they don’t know how much tax they will need to pay to ship the grain as Moscow steps up its fight to curb domestic food inflation. Russia will launch a formula-based wheat export tax from June 2 aimed at cooling domestic grain prices. It will be set weekly and will replace the current fixed tax of 50 euros ($60) a tonne.

Russian wheat yield forecasts remain high despite lagging vegetation density – Refinitiv Commodities Research

—Favorable recent weather maintains 2021/22 Russia wheat production at 78.6 [68.5–91.0] million tons. Mostly mild weather continues to indicate strong yield potential, although some areas could still show poor regrowth due to winterkill, particularly in portions of the far South and Central District.

Ukraine wheat production outlooks unchanged as cold and wet spring weather continues – Refinitiv Commodities Research

Healthy soil moisture levels maintain Ukraine rapeseed production despite cool spring weather – Refinitiv Commodities Research

Ukraine’s economy ministry has proposed banning exports of sunflower seeds from May 15 to Sept. 30, 2021, despite its insignificant volume, the ministry’s draft resolution showed. Ukraine, the world’s major exporter of sunflower oil, this week limited sunoil exports to 5.38 million tonnes in the 2020/21 season in a bid to prevent a jump in sunoil prices on domestic market.

Concerns remain due to potential freeze damage for EU-27 + UK rapeseed crops – Refinitiv Commodities Research

—With cold and dry weather still dominating in recent weeks, improved weather prospects into May tentatively maintain 2021/22 EU-27 + UK rapeseed production at 18.3 [17.1–21.4] million tons (mmt).

Euronext wheat extended gains on Wednesday, with new-crop positions again hitting contract highs, as adverse crop weather in North and South America sustained a rally in grain markets. September milling wheat settled up 3.00 euros, or 1.4%, at 213.25 euros ($256.56) a tonne, after earlier reaching a new life-of-contract peak at 214.25 euros.

Rapeseed also remained supported by tensions in global oilseed markets and concern about weather damage to crops in Europe. New-crop August rapeseed set a new contract high at 504.75 euros before settling up 1.3% at 502.50 euros.

India’s edible oil industry is taking measures to avoid any shortage of workers as mustard harvesting and soybean crushing are in full swing. Increasing Covid-19 cases and imposition of tighter restrictions including lockdown in some states have created anxiety among migrant workers and the industry is seeking to allay their fears. Company executives said they are arranging food and housing for the workers in factory premises and vaccination camps for those who are aged 45 years and above so that they can work in the fields and factories.