Written Commentary

>>Read the complete, in-depth May 2026 Edition HERE

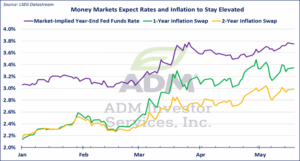

The core challenge for gold during is the same dynamic that pressured prices in March, but it has intensified. With April CPI reaching 3.8% YoY and core CPI at 2.8%, headline inflation is running nearly double the Fed’s 2% target, which would normally be constructive for gold as an inflation hedge.

Interested in more futures market commentary? Explore our Market Dashboards here.