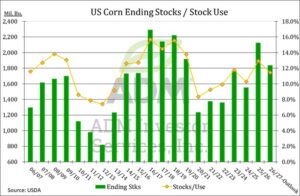

USDA February WASDE lowered US 2025/26 corn stocks to 2.127 billion, down 100 million.

Ending stocks still a seven-year high, stocks/use ratio at 12.9% a six-year high.

Exports raised 100 million bushels to a record 3.30 billion. No change to ethanol or feed/residual usage.

Bulls disappointed with lack progress with E-15 year-round sales.

SOYBEANS

USDA February WASDE saw no changes to the 2025/26 balance sheets for the entire complex.

Ending stocks at 350 million bushels are holding at a seven-year high

Without additional Chinese buying, the USDA export forecast at 1.575 billion bushels appears high.

The current crush pace supports a 10-20 million-bushel increase to the USDA estimate of 2.570 billion.

WHEAT

USDA February WASDE saw US 2025/26 ending stocks at 931 million bushels, up 5 million from the January update and a six-year high.

Hard Red Spring (MIAX) food usage was lowered by 5 million bushels.

Global ending stocks were lowered by nearly 1 million metric tons to 277.5 million.

Argentine exports were revised up by 2 million metric tons to 18 million; Canada was up 1 million to 29 million.

COCOA

Cocoa supplies backing up in Ivory Coast and Ghana after both countries raised their official farmgate prices last year, which encouraged production but left buyers unwilling to pay at those levels. Ghana has already cut its price, and Ivory Coast is considering doing so as well.

Ivory Coast’s January cocoa grind was – 2.1% from the previous year, and their cumulative grind since the season began in October was down 7.4%

When prices went to almost $13,000 metric ton in 2024, candy and cookie manufacturers looked to alternative products, either using less chocolate or none at all. Halloween 2025 was the “Year of the Gummy Bear.” These manufacturers buy in advance, so it took a while for the high prices to reach down to the manufacturer.

COFFEE

May Coffee broke below a five-month consolidation in late January and it has since moved into a consolidation area established last July.

Brazil’s 2026 looks promising. This is the “on-year” in the biennial cycle for their arabica crop, and the key growing region has seen good rainfall this season after a dry start last fall. Forecasts range from 44.1 to 48.0 million bags for arabica (median 45.75 million) versus a median of 35.8 million for 2025.

SUGAR

The large global surplus for 2025/26 has sent sugar prices to their lowest level in more than five years. However, analysts speaking at the Dubai Sugar Conference in February called for global surplus of 1.4 million metric tons in 2026/27, not as large the 4.7 million for 2025/26.

Low sugar prices are expected to discourage beet plantings in 2026/27. The Brazilian cooperative Tereos put EU planted are down 6%-7%, and Czarnikow forecast a 5% decline.

Low sugar prices are also encouraging cane crushers to focus more on ethanol production than sugar. The UNICA sugar’s share of the crush fell to 6.6% in Center-South Brazil for the second half of January versus 23.6% for the same period last year. Crushing activity in a seasonally slow period, which means the overall impact on production volume is minimal. Still, the sharp drop in sugar’s share of crush is noticeable.

COTTON

May Cotton bounced off contract lows in early February and managed an impressive rally the during the third week of the month.

At their annual Outlook Conference, USDA economists put US 2026/27 cotton plantings at 9.4 million acres, down from 9.75 million in their baseline projections last fall and up from 9.28 million in 2025/26.

The USDA Supply/Demand report in February left US 2025/26 cotton production unchanged from the January estimate, but exports were lowered by 200,000 bales, resulting in a 200,000-bale increase in ending stocks. This put the stocks/use ratio at 32.4% versus 30.4% in January, and the highest the ratio has been since 2019/20, when it reached 42.7%.

CRUDE OIL

The US build-up of warships around the Persian Gulf have raised increased the chances of a US attack on Iran. President Trump has stated that “really bad things” would happen if Iran does not come to an agreement to curtail its nuclear program, but he also mentioned a deadline of 10 to 15 days, which may have made the attacks appear less imminent than they had prior to his comments.

A primary concerns to oil traders is that Iran may respond to US attacks by closing the Strait of Hormuz, through which about 20% of global oil supply passes. They have also threatened US military bases in the region.

NATURAL GAS

April Natural Gas rallied from a 5 ½-month low of $2.604 on January 9 to $4.085 on January 30 on an extreme cold weather event in the eastern half of the US in late January that extended from the Canadian border to Mexico and the Gulf. However, the cold was short-lived, and the market has since given back 82% of the rally.

US gas in storage fell a record 360 billion cubic feet during the week ending January 30, and that and two subsequent weeks of larger-than-normal withdrawals helped pull US storage to a 3.6% deficit to 2025 for the week ending February 6. This was the first time supply was at a deficit since the beginning of the year.

The extreme in January cold also caused freeze-offs at wells, reducing US gas production in January to an average of 106.3 billion cubic feet per day from a record 109.7 bcfd in December. Production has since come back on line, reaching an for February at 109.7 bcfd as of the February 20.

LIVE CATTLE

Beef wholesale prices gained 14% to 16% in 2025.

Despite beef retail prices gaining +19.3% in 2025, the February USDA WASDE Report indicated US beef consumption increased 0.1% to 59.2 pounds per person. It is expected to grow to 59.5 pounds in 2026.

Live Cattle plummeted after President Trump announced beef quotas doubling from Argentina but have since recouped their losses

LEAN HOGS

US pork consumption in 2025 was disappointing, as many analysts had expected it to increase due to high beef prices.

The February USDA WASDE Report put per capita consumption at 49.3 pounds, down from 49.9 pounds in 2024. However, 2026 consumption is expected to climb to 50.5 pounds per person.

Pork prices have increased in 2026. The CME Lean Hog Index began the year at $82.26 and moved up to $86.38 through January. As of February 18, it was up to $87.13.

STOCK INDEX FUTURES

Volatility has weighed on equity indexes in recent weeks, as renewed concerns over the durability of legacy and enterprise software models emerged following rapid developments in the AI space.

Advances in AI applications — particularly within legal and data-processing tools — raised fears that portions of enterprise software demand would be displaced by automation, prompting a rotation out of technology shares and into more “AI-insulated” sectors such as utilities, consumer staples, mining, construction, and telecommunications.

Between January 20 and February 17, the S&P 500 declined roughly 1.1% and the Nasdaq nearly 3.7%, while the Dow Jones Industrial Average advanced about 0.5% after briefly surpassing the 50,000 level, highlighting a divergence between growth-oriented and defensive segments of the market.

CURRENCIES

The US Dollar Index has declined roughly 2.2% since January 20. It not made a move above 100 since November, and it continues to encounter resistance near 96.20.

Fed Policy expectations are largely unchanged, with markets pricing in two rate cuts this year. January CPI and NFP figure were bearish to prices, but expectations of an extended pause from the Fed leave the dollar subject to rangebound action ahead of economic data.

The euro has strengthened roughly 2% against the dollar to $1.185, as the currency has drawn support from indications that the European Central Bank remains comfortable with the currency’s recent appreciation. Reports that Bank of France Governor François Villeroy de Galhau is expected to step down in June is viewed as marginally hawkish given his typically dovish stance. It continues to draw structural support from capital flows and relative equity performance despite a neutral policy backdrop.

INTEREST RATES

US Treasury yields have fallen alongside a substantial flattening in the curve, reversing a strong steepening move from late January to early February. Yields have come under pressure from January’s CPI print, which reinforced a broader disinflation trend but revealed pockets of sticky inflation.

Headline CPI price growth eased to 2.4% in January from 2.7% in December, while core prices eased to 2.5% from 2.6%. On a monthly basis, core prices rose 0.3% versus December’s 0.2%.

January’s strong nonfarm payrolls bolstered support for FOMC hawks, as the data pointed to a stable labor market. Unemployment edged down to 4.3%, even as the labor force participation rate increased from 62.4% to 62.5%, reinforcing the narrative of a low-hire/low-fire environment. Broader labor supply dynamics remain a point of uncertainty, particularly as Trump administration policies on immigration are likely to weigh on net workforce growth.

GOLD & SILVER

April Gold has traded in a consolidated range since early February and up until the Supreme Court decision on the Trump tariffs, was unable to sustain a move above $5,000.

On January 30, April Gold saw a spectacular decline from $5,440 to $4,700 after strong selling in China triggered institutional selling worldwide, as banks were forced to protect gains, the CME increased margin requirements, and retail investors were forced to sell as a result.

Silver recorded a more dramatic collapse, closing at $78.53 that day after peaking at $121.79 the day before. The silver, platinum and palladium markets are smaller and less liquid, making them more vulnerable to speculative flows.

COPPER

US copper futures have fallen roughly 0.5% as warehouse levels across the LME, SHFE, and COMEX. Copper stocks in LME warehouses have reached 224,625 metric tons and are up about 70% since the beginning of the year. Shanghai stocks are also increasing, having reached 272,475 tons, while COMEX stocks are holding steady around 538,000 tons.

Copper flows to the US have remained strong in anticipation that further US tariffs will be announced in mid-2026 and implemented in 2027. (They were not affected by the US Supreme Court decision.) That dynamic had been supporting LME-COMEX arbitrage, but as US inventories grew to more than 500,000 tons and as LME stocks above 200,000, arbitrage opportunities faded.

Interested in more futures market commentary? Explore our Market Dashboards here.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.