Written Commentary

>>Read the complete April 2025 Edition HERE

Prices rebounded nicely the first half of April as corn seems to be least impacted from the Trump Administration’ tariff policies. Demand for U.S. corn remains strong evident by the USDA 100 mil. bu. increase in its export forecast to 2.55 bil. bu. Overall, U.S. ending stocks were cut 75 mil. bu. to 1.465 bil. as feed usage was lowered by 25 mil. bu. The new ending stocks forecast was roughly 50 mil. below pre-report estimates.

Prices across the soybean complex have also rebounded nicely off the early April lows, shaking off pressure from escalated trade tensions with China. While China has reportedly bought upwards of 50-60 cargoes of soybeans from Brazil in the past week, this happens every year as their demand shifts to our South American competitors. The USDA cut U.S. soybean stocks 5 mil. bu. to 375 mil. While the USDA data may not have been bullish, it certainly wasn’t bearish.

Wheat prices have shown only a limited bounce off their March lows, despite speculative traders holding a near record large short position. The USDA increased their ending stocks forecast by 25 mil. bu. to 846 mil. in the April 2025 WASDE report, 20 mil. above expectations. Imports rose 10 mil. bu. while exports were lowered by 15 mil. HRW stocks jumped 26 mil., spring wheat stocks rose 16 mil., while durum stocks were down 13 mil. SRW wheat stocks (CGO) held steady at 116 mil. bu.

In early April, Ivory Coast officials warned that the nation was about to experience its worst mid-crop in at least 10 years due to an unusually long dry season, and Ivory Coast also raised the fixed farmgate price paid to cocoa farmers by 22% to 2,200 CFA francs ($3.65) per kilogram for the mid-crop of the new 2024/25 season. season. A couple of days later President Donald Trump said he would impose a 10% baseline tariff on all U.S. imports, taking the maximum to more than 50% for some countries. This sparked a three-day selloff back taking prices to long term support at the 200-day moving average. Ivory Coast port arrivals recovered to 15,000 metric tons for the week ending April 13 after falling to 1,500 the previous week.

NY (arabica) coffee traded to new all-time highs in February and proceeded to consolidate its gains over the next two months before breaking out to the downside of a triangle formation, which could be an indicator of a major top. This selloff was aided by the tariff announcements, which included an extremely high rate against Vietnam, the world’s largest robusta producer and a major supplier to the U.S.

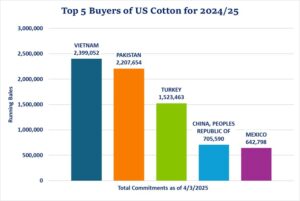

Cotton prices fell precipitously in the immediate aftermath of the reciprocal tariff announcements at the beginning of April, as the largest buyer of U.S. cotton this year, Vietnam, was hit with one of the biggest tariff rates. When President Donald Trump postponed the implementation of the tariffs, traders breathed a sigh of relief. But even before that announcement was made, Vietnam had expressed a willingness to commit to buying more U.S. liquified natural gas in an attempt to reduce its trade surplus with the U.S. and negotiate a lower tariff rate.

The recent UNICA report showed Brazilian Center-South sugar production for the second half of March was at 201,000 tons, up from 183,000 a year ago and up from 53,000 for the first half of the month. This was the first time product was above year ago levels since October. Sugar’s share of the crush was 43.0% versus 33.5% for the same period last year, and there were 44.13 kilograms of sugar produced per ton of cane during the second half of March versus 35.86 kilograms a year prior.

Crude oil prices collapsed in the wake of the reciprocal tariff announcements on April 2, as the size of the tariffs far exceeded expectations and raised fears of a global recession. The weekend after the tariffs were announced, Saudi Arabia cut its benchmark price for Asia, which added to selling pressure. June crude oil prices fell from $71.23 per barrel at the close on April 2 to $55.67 at its low on April 9, a 23% decline in one week. Nearby prices fell to their lowest level since February 2021. The market put in a spike low on April 9 after President Donald Trump announced a 90-day delay in the implementation of the tariffs, but the potential for a sharp decline in global oil demand if the event of an economic slowdown looms over the market.

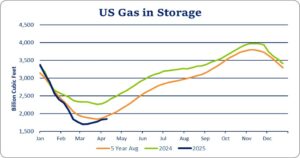

The natural gas market peaked in early March at the height of rhetoric between the Trump Administration and Canada over the tariffs, which at that point included U.S. tariffs on imports of Canadian crude oil and natural gas and threats by the Ontario premier to suspend electrical supply to the U.S., which would increase U.S. gas demand even further. The subsequent selloff coincided with five straight weeks of larger than normal U.S. storage builds, which allowed U.S. supply to narrow its deficit from year ago levels.

Traders at the start of March 2025 were expecting tariffs to begin with China, Mexico and Canada. With the first round of tariffs announced President Trump within two days announced a delay until April for Mexico and tariffs for Canada would remain the same as when President Trump made the trade agreements during his first term in office, which President Biden did not change. Tariffs for China would be 10% above previous tariffs. Not increasing tariffs for Mexican products was important because it meant allowing feeder cattle to enter U.S. feedlots after the delay of Mexican feeder cattle and quarantine due to New World Screwworm placed at the beginning of 2025 and the quarantine lifted at the end of February 2025.

Trading after a steep decline from February 18 to March 4, lean hogs rebounded close to $8.00 and traded sideways to slightly lower the remainder of the month. The Quarterly Hogs and Pigs report on March 27 showed All Hogs as of March 1 were slightly lower than the same period in 2024. Hogs kept for breeding were down 2% and hogs kept for market were down slightly. Similar to previous reports, due to better management and genetics, pigs per litter were up 1%. Producers for March through May intend to farrow the same amount of sows as they did a year ago. From the producer side, hog numbers should be similar to 2024.

Stock index futures came under pressure as investors prepared for another week of developments on President Donald Trump’s tariff policies and for the kickoff of large tech company earnings reports. In addition, there are concerns about the Federal Reserve’s independence.

March U.S. dollar index futures fell to a three-year low due to concerns about the economic outlook for the U.S., along with renewed concerns over the Federal Reserve’s independence. The greenback has lost approximately 4.6%, with its steepest declines against the euro currency, the Japanese yen, and Swiss franc.

The euro currency advanced to its strongest level since November 2021. There was virtually no negative reaction to news that the European Central Bank lowered its key interest rate by 25 basis points at its monetary policy meeting.

GOLD

June gold futures advanced to record highs. Recent gains can be attributed to safe-haven demand in light of ongoing uncertainty around U.S. trade policy. Markets remain sensitive to fluctuating tariff news, with the Trump administration launching trade probes that could lead to new tariffs on semiconductor and pharmaceutical imports.

Interested in more futures market commentary? Explore our Market Dashboards here.