Written Commentary

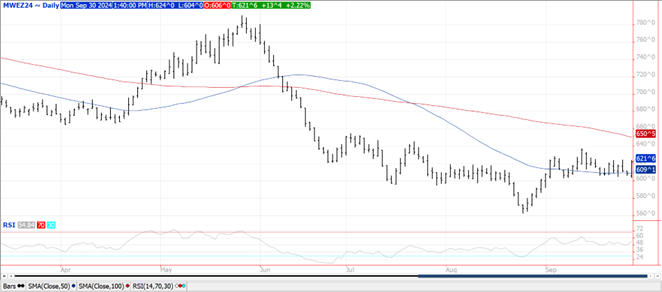

Sept. 1st stocks at 1.760 bil. were 93 mil. bu. below pre-report estimates and down 52 mil. bu. from Aug-24 USDA WASDE report. Today’s data would suggest stronger than expected feed usage in Q4 of the 2023/24 MY. 780 mil. bu. were held on-farm representing 5% of 2023 crop, the highest in 4 years. Adjusting the lower carry-in stocks from 2023/24 would reduce new crop ending stocks to just above 2.0 bil. bu. holding all other variables constant. Export inspections at 45 mil. bu. were at the high end of expectations and in line with the weekly amount needed to reach the USDA forecast of 2.30 bil. bu. YTD inspections at 131 mil. are up 24% from YA vs. the USDA forecast of up less than 1%. Last week money managers were net buyers of just over 4k contracts reducing their short position to just below 131k, the smallest in 4 months. While Canada’s Grain Workers Union has reached a tentative agreement to end a work stoppage in Vancouver the US braces for port strikes along the East and Gulf coasts starting tomorrow. AgRural reports that Brazil’s 1st corn crop plantings has reached 30%. Dec-24 corn briefly traded above the July high of $4.26 ½ with next resistance at the 100 day MA of $4.29 ¼. While spreads remain historically wide they have narrowed nicely from the mid-August lows.

Sept. 1st stocks at 342 mil. were 8 mil. bu. below pre-report estimates, up only 2 mil. bu. from Aug-24 USDA WASDE report. Last year’s crop was trimmed 3 mil. bu. to 4.162 bil. Remnants of Hurricane Helene are still impacting regions of the ECB for the next 24 hours. Dry and warmer conditions have favored harvest activities in the western half of the Midwest. Hot/dry conditions continue to dominate northern growing regions of Brazil however forecasts suggest beneficial rains will arrive starting week 2 of October. Export inspections at 25 mil. bu. were in line with expectations however below the 34 mil. needed per week to reach the USDA forecast of 1.850 bil. bu. YTD inspections at 71 mil. are down 3% from YA vs. the USDA forecast of up 9%. China took just over 7 mil. with 5 mil. going to Germany. Last week money managers were net buyers of just over 47k contracts of beans reducing their short position to 75k contracts, smallest in 3 months. MM’s were also net buyers of nearly 32k bean oil and 18,500 soybean meal. AgRural reports that Brazil’s soybean crop is 2% planted, vs. 5% YA. Today’s EIA data showed biodiesel and RD capacity actually dropped nearly 300 mil. gallon in July to 6.620 bil. gallons with all of the decline coming from renewable diesel. Combined production of biodiesel and RD dropped 1.3% in July to 458 mil. gallons., still the 2nd highest monthly production figure ever reported. Bean oil usage for biofuel production slipped to 1.139 bil. lbs., down 10% from June and down 10.5% from July-23. In the first 10 months of the 24/25 MY bean oil usage has reached 10.691 bil. lbs. up 6% from YA vs. the USDA forecast of up 4%. To reach the current USDA forecast of 13.0 bil. lbs. bean oil usage in August and Sept will need to reach an average of 1.155 bil. lbs. per month vs. the 3 month average of 1.161 bil. Nov-24 beans were able to scratch out a fresh 2 month high however failed to challenge the 100 day MA at $10.78 ½. Dec-24 meal reached a fresh 3 month high before pulling back.

Sept. 1st stocks at 1.986 bil. bu. were slightly above expectations and well above the 1.767 bil. from YA. All wheat production slipped 11 mil. bu. to 1.971 bil. roughly 13 mil. bu. below the Ave. trade guess. Winter wheat production at 1.349 bil. was down 12 mil. vs. expectations for no change. HRW was cut 6 mil. to 770 mil., SRW unchanged at 342 mil. while white winter was down 7 mil. to 236 mil. Spring wheat was cut 2 mil. to 542 mil. bu. Sept 1st stocks/implied Q1 usage at 2.77 us slight above the 2.71 from YA despite stocks being well above YA. Winter wheat production was an 8 year high. Export inspections at 20 mil. bu. were in line with expectations and above the 15 mil. needed per week to reach the USDA forecast. YTD inspections at 303 mil. are up 35% from YA, vs. the USDA forecast of up 17%. The Philippines were the largest taker with 9 mil. bu. MM’s were lite sellers in Chicago and KC futures last week while being a small buyer of MGEX wheat.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.