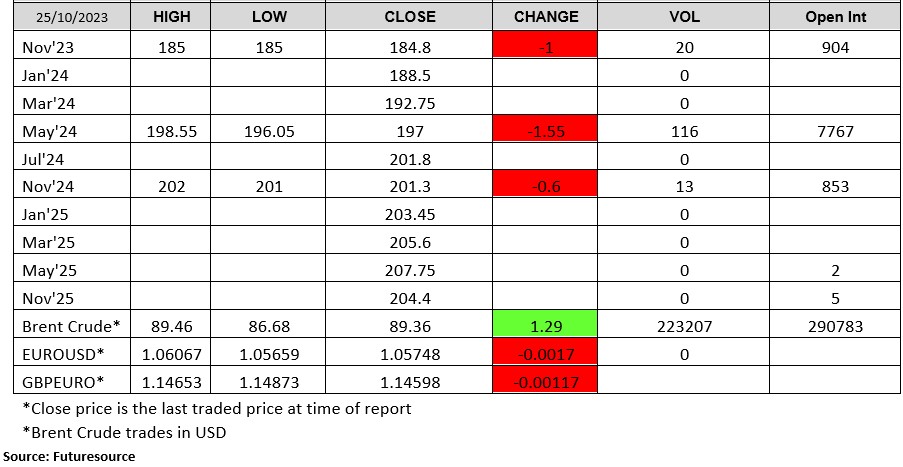

Written Commentary

Futures were $.05 – $.06 lower today making new lows late in the session. Dec-23 closed below the 50 day MA support at $4.85 ½, however held above the Oct. 12th low (USDA report day) of $4.82 ¼. Heavy rains are expected over the next 5–7 days moving NE from the US southern plains thru the central Midwest producing 1-3” rainfall totals. States most impacted by corn harvest delays will be MO, IA, IL, WI, MI, and IN. The rains however will help raise water levels across the lower Mississippi. The USDA did announce the sale of 117k mt (4.6 mil. bu.) of corn to Mexico. US harvest progress advanced 14% last week to 59% matching the YA pace while staying above the 5-year Ave. of 54%. Since Ukraine started utilizing the “Humanitarian Corridor” in August along the western Black Sea coastline they have been able to export 700k tons of agricultural products along this route. Ukraine’s Ag. Ministry still expects export volumes will reach 2.5 mmt a month utilizing the corridor and the Danube River thru neighboring Romania. As of Oct. 22nd the EU has imported 5.45 mmt of corn, down 40% from YA. While US ethanol margins have retreated in recent weeks they remain historically strong. The range of estimates for tomorrow’s EIA weekly ethanol production report is 1,000 – 1,050 tbd vs. 1,035 tbd the previous week.

The soybean complex was mixed with beans up $.06-$.09 making new highs in late trade. Meal was $8-$14 higher led by spot Dec-23 which made a 7 month high. Next resistance is the Mch-23 high at 437.70. Comments that Argentina may run out of soybeans to crush in November helped fuel the surge. Oil was 60-75 lower with Dec-23 trading to a new 4 month low. Next support is at $.50 lb. Spot board crush margins jumped $.15 today to $2.24 ½ bu. the highest in 5 weeks. Meal product value reached 63%, this highest since May-23. Following good rain in key growing areas of Argentina over the weekend another round of precipitation is forecast for the late this weekend into early next week. Scattered rains are likely for WC Brazil late this week and weekend however will likely not be enough to offset evaporation loss from much above normal temperatures. There are chances for daily showers across southern Brazil over the next week to 10 days which could provide another 3-5” across the already soaked region. US harvest progress has reached 76%, having fallen just below the YA pace of 78% however ahead of the 5-year Ave. of 67%. The US Soybean Export Council this morning announced that Chinese importers signed 11 non-binding frame contracts to purchase “billions” worth of US agricultural goods. No volume figures were provided however this was their first signing in years. There were no export sales were announced. EU soybean imports since July 1st have reached 3.35 mmt, just a touch below the 3.44 mmt from YA.

Prices were $.06 – $.10 lower across all 3 classes today. KC Dec-23 held above its contract low at $6.55 ¼. Rumors of Chinese interest in US wheat helped prices rally early yesterday, only to fail in late day trade. There were no sales announced this AM. Also weighing on prices are reports that Commerzbank raised their Australian wheat production est. 3 mmt to 26-28 mmt due to beneficial rains earlier in Oct. In October the USDA lowered their Australian production forecast 1.5 mmt to 24.5 mmt. Ukraine’s Ag. Ministry reports 79% of their winter wheat crop has been planted, and 79% of all their winter crops have been sown. EU soft wheat exports as of Oct. 22nd have reached 9.33 mmt, down 22% from YA. US winter wheat plantings have reached 77%, in line with YA and the 5-year Ave. Emergence has reached 53%.

See more market commentary here.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.