Written Commentary

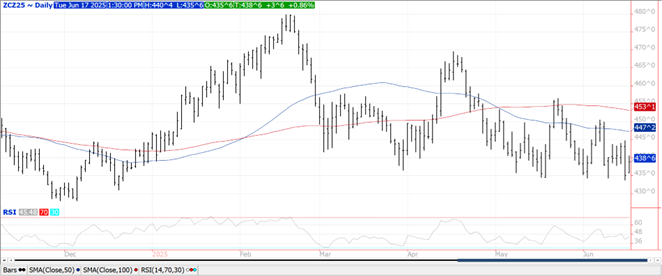

Prices ranged from down $.03 in spot July to up $.04 in new crop as spreads weakened. July fell back to a $.07 discount to Dec-25 pressured by easing Gulf basis levels. July-25 did hold support above LW’s low at $4.29 ¼. Inside trade for Dec-25. Ratings improved 1% to 72% G/E in line with expectations. Conditions improved in 9 states, declined in 7 while holding steady in 2. Overall ratings remain slightly above their historical average. EU corn imports for 24/25 as of June 15th at 19 mmt are up 6% from YA. With a few weeks left in the old crop MY EU corn imports will likely come in very close to the USDA forecast of 20 mmt. Funds sold roughly 21k contracts yesterday extending their short position to over 190k for the 1st time since Aug. Tomorrow’s EIA report is expected to show ethanol production range between 329-331 mil. gallons, holding at or above the previous week’s record production of 329 mil. gallons. The market continues to shrug off tight global stocks as strong demand shifts toward SA origin. IMO at these price levels the market is discounting higher, possibly much higher 2nd crop production in Brazil helping ease the global supply tightness. Growing crop prospects here in the US is also weighing on market sentiment.

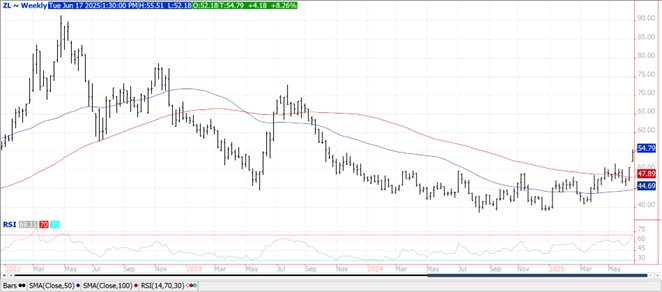

Prices were mixed across the complex today. Beans ranged from $.04-$.08 higher, meal was $1-$2 better while bean oil slipped 20-30 points. July-25 beans rejected trade below yesterday’s low setting up today’s bounce. Nov-25 beans traded to a fresh 4 ½ month high with next resistance at $10.75 ¾. A new 20 month high for July-25 oil before correcting. New contract low for July-25 meal before bouncing. Next support is at $278.50. The lower price has uncovered some export demand as the USDA announced the sale of 120k mt of meal to an unknown buyer. Crush margins took a breather today backing off $.05 in the spot contracts to $1.56 bu. with bean oil PV slipping to 49%. New crop margins dropped $.03 ½ to $1.98 bu. US weather is mostly favorable with much of the nation’s midsection expected to receive .75-2” of rain this week. Extreme heat will impact the WCB and southern plains with at least a couple of days of triple digit heat for KS and W. NE by late this week. Extended forecasts show some cooling in the WCB for the last week of June with above normal temps to remain for the east. Normal to above normal precipitation is expected across the continental US. Soybean plantings advanced only 3% to 93% complete, vs. 92% YA and the 5-year Ave. of 94%. According to USDA data there remains just over 5.8 mil. acres of soybeans left to plant. Over 2.3 mil. acres are in IL, IN, OH, and MO where the final planting dates for crop insurance on June 20th is quickly approaching. The slow pace to winter wheat harvest has also contributed to the slower soybean plantings in double crop areas. The market is attempting to give US farmers the incentive to get these acres planted in the event trendline yields are not attained resulting in a considerably tight balance sheet. Crop ratings declined 2% to 66% G/E while expectations were for a 1% improvement. Ratings improved in only 4 states, declined in 11 while holding steady in 3. Biggest declines were in LA and MI both down 9% while WI was down 7%. EU soybean imports as of June 15th at 13.6 mmt are up 7% from YA. Meal imports at 18.6 mmt are up 26.5% YOY.

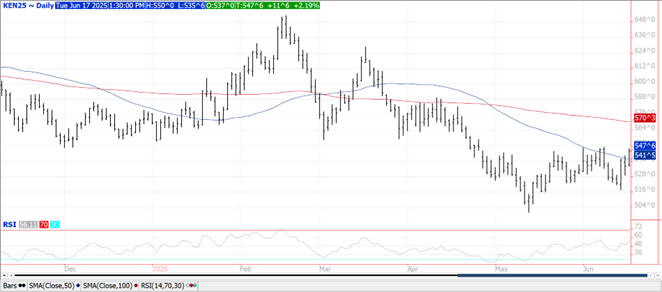

Prices ranged from $.08 higher in MGEX to $.13 better in CGO. July-25 CGO and KC reached their highest price level in a week. Near term resistance rests at $5.57 ¾ for CGO and $5.51 for KC. Winter wheat ratings slipped 2% to 52% G/E vs. expectations for no change. The percentage of the crop rated poor or VP increased 3% to 19% as there was also a 1% drop in fair. Despite the drop, overall ratings are still above their 5-year Ave. Conditions improved in only 3 states, declined in 13 while holding steady in 2. Harvest advanced 6% to 10% complete, the slowest in 4 years and well below the 25% YA and 5-year Ave. of 16%. Spring wheat conditions improved 4% to 57% G/E, above expectations. With the improvement overall conditions are slightly above their 5-year Ave. Wire services are reporting Algeria has bought between 550k-570k mt of milling wheat at their nominal tender for only 50k mt. Prices are reportedly near $244.50 – $245/mt CF with most of the grain sourced from the Black Sea region for July/Aug shipment.

Charts provided by QST.

>>See more market commentary here.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.