Written Commentary

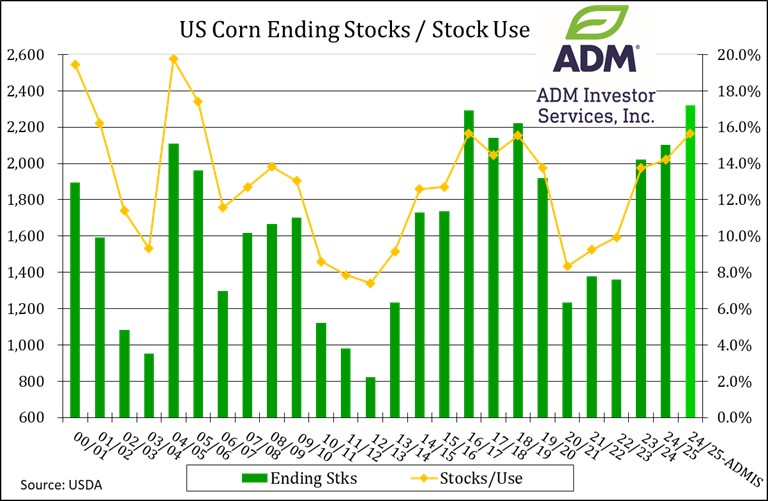

Prices are mixed as spreads firmed. Sept-24 was up $.02 after carving out a new contract low in early trade however was not able to forge a key reversal day. Dec-24 and beyond were $.01-$.03 lower. Export news is lacking despite the plunge in price. Ethanol production dropped 1,054 tbd down from 1,064 tbd the previous week however up 2% YOY. Production was slightly below the pace needed to reach the USDA corn usage forecast of 5.450 bil. bu. There was 105.6 mil. bu. of corn used, or 15.1 mil. bu. per day, below the 15.33 mbd needed to reach the USDA. Ethanol stocks held steady at 23.6 mil. barrels, up from 22.7 mb YA. Implied gasoline usage last week at 9.398 mbd was down slightly for the week, however up 7.3% from YA. Conab to release updated Brazilian production forecast’s tomorrow morning. Export sales tomorrow are expected to range from 15 – 50 mil. bu. for both crop years combined

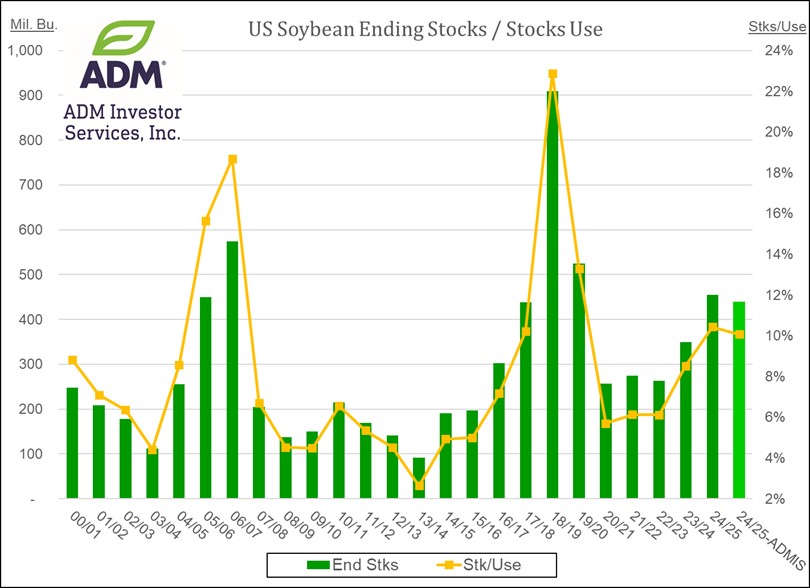

The soybean complex was lower across the board with beans down $.13-$.18, meal was $2-$6 lower while oil finished weak down 60-70 following 2 sided early trade. Both Aug-24 and Sept-24 beans established new contract lows while new crop Nov-24 traded to a 3 year low. Spreads have weakened for beans and meal. Next support for Aug-24 is $11.00. Next support for Aug-24 oil is the 100 day MA at $.46. Aug-24 meal traded to a 2 ½ month low with next support just above $330. Spot board crush margins (Aug-24) backed off a few cents today to $1.43 bu. As remnants of Hurricane Beryl exit the Great Lakes region in the next 24-36 hours a dryer pattern is expected for much of the nation’s midsection for the next week. Temperatures are expected to build to low 90’s for the central and ECB, upper 90’s low 100’s for the WCB and plain states. For now no immediate concern with above normal temperatures as much of the crop areas have been well-watered. That could change if heat/dryness extend into late July/early Aug. The USDA announced the sale of 132k mt (4.8 mil. bu.) of 24/25 soybeans to China, the first known new crop purchases by the Asian country. The Chinese purchase wasn’t able to alter the bearish sentiment as US crop prospects grow and speculative traders continue to pile on the short side of the trade. Export sales tomorrow are expected to range from 10 – 30 mil. bu. for beans, 200-600k tons meal, and 5-20k tons of oil.

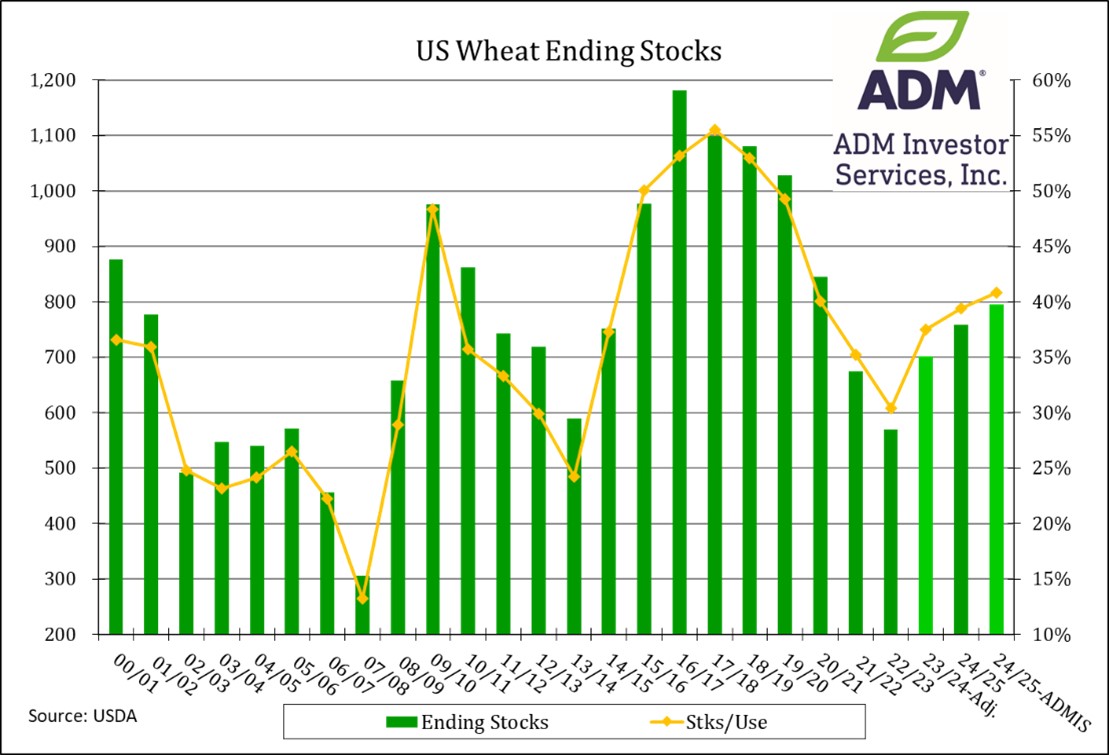

Prices were lower across all 3 classes today as markets brace for higher US production in Friday’s USDA reports. Chicago and KC were $.10-$.12 lower while MGEX is down $.06-$.07. Sept-24 Chicago violated support at the June low, however recovered to close above $5.60. Sept-24 KC fell to a 4 month low with next support at the contract low of $5.52. Reports of a Russian missile strike causing infrastructure damage on an Odesa port while also killing a security guard and truck driver was able provide a price boost. A South Korean milling group bought a combined 90k mt of US and Canadian wheat for Sept shipment. Jordan passed again on their most recent 120k mt tender, however issued another 120k mt tender with a July 16th deadline. All wheat production on Friday is expected to reach 1.915 bil. bu. up 40 mil. from June. Exports tomorrow are expected to range from 12–25 mil. bu.

>>See more market commentary here.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.