Written Commentary

SOYBEANS

Soybeans ended higher. SH range was 14.65-14.92 and ended near 14.84.

Combination of dry Argentina and S Brazil weather forecast and lower than expected CPI inflation numbers supported soybean futures. Higher energy prices helped soyoil futures traded higher and also supported soybean futures. Soybeans had traded lower on Monday due to Central Argentina rains. Argentina and S Brazil 10 day weather forecast is dry. Estimates for Brazil soybean crop is 151-160 mmt vs USDA 152 and 127 ly. Estimates for Argentina soybean crop is 44-50 mmt vs USDA 49.5 and 43.9 ly. Most still feel US soybean exports could drop from USDA number, This offers resistance to prices. Fact SH is higher that SX23 reflects tight old crop US supply versus ideas US farmers will increase 2023 acres and trend yield will add to end stocks and weigh on futures.

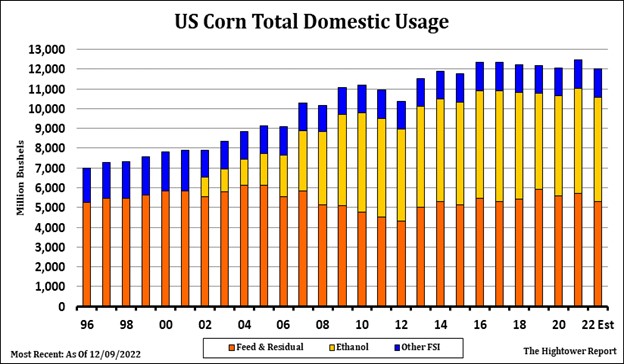

CORN

Corn futures ended sharply unchanged. Financial markets are trying to decide if lower than expected CPI inflation data and some looking for Fed to slow interest rate hikes is more important that slowing US and global economies. This weeks Fed Chairman comments could be key for direction of equities, US Dollar and energies. Corn futures have to decide if dry Argentina and south Brazil weather and slow US farmer selling is more important than slow US exports and increase Brail and Ukraine exports. Some Fear recent bombing of Odesa and slowdown in Russia exports could support futures. Drop in domestic ethanol margins and talk EV and recession could slow gas and ethanol demand offers resistance. Some estimate Argentina corn crop as low as 43 mmt vs USDA 55, There are no Brazil corn export prices after January. Rains in central south US is helping logistics but Cold weather next week could slow grains movement. Some Look for lower hog prices due to lower exports. Same group could see lower Q123 cattle futures due to increase competition for US exports. Lower US cattle number could rally cattle futures after Q123.

WHEAT

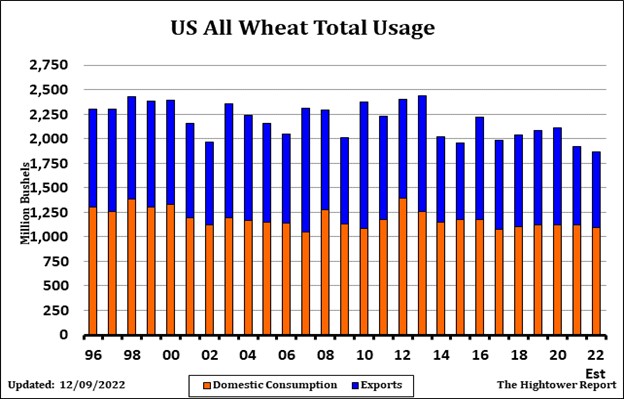

Wheat ended mixed with Mpls and KC gaining on Chicago. USDA est US 2022/23 HRW end stocks near 259 mil bu vs 360 ly. Some look for 2023 HRW crop near 635 mil bu and end stocks at 220. This assumes better US south plains weather and now increase in exports. HRS 2022/23 end stocks are est near 124 vs 139 last year. Same group could see 2023 US crop near 485 and end stocks near 150. HRS futures still are a premium to HRW on increase demand for protein. US SRW 2022/23 end stocks are est at 87 vs 94 lt. US 2023 crop is est near 357 and end Stocks near 110. Mpls should gain on HRW and SRW, Matif closed slightly lower as the €uro hit a 6-month high. Increase French vessel line-up explains cash strength, in particular the Chinese volume. Brussels’ shipment update shows a 6 pct increase vs last year. Ukraine Grain Traders Union (UGA) asked the Govt to prioritize electricity to grain silos. Iraq is in for US/Canadian/Aussie.

See more market commentary here.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.