Written Commentary

Prices range from $.01-$.07 higher today led by old crop futures. Spreads firmed as deliveries against May futures at only 25 contracts were below expectations. Most actively traded July was back testing its 50 & 100 day MA today, however unable to penetrate. Global weather remains largely favorable. Looking out to mid-May above normal temperatures are expected across much of the nation’s midsection with above normal precipitation for the WCB, below normal for the east. The USDA announced the sale of 120k mt (4.7 mil. bu.) to an unknown buyer. Ethanol production rebounded to 1,040 tbd, or 306 mil. gallons, up from 304 mil. the previous week, and up 5% YOY. There was 104 mil. bu. used in the production process, or 14.9 mil. bu. per day, in line with the amount needed to reach the USDA forecast of 5.50 bil. bu. In the MY to date there has been 3.596 bil. bu. used, or 15.17 mbd, an annualized pace of 5.538 bil. Implied gasoline usage slipped 3.4% LW to 9.1 mbd however still 5.6% above YA. Ethanol stocks slipped to 25.4 mil. barrels, slightly below expectations and the lowest in 15 weeks. Tomorrow’s export sales are expected to range from 30-65 mil. bu.

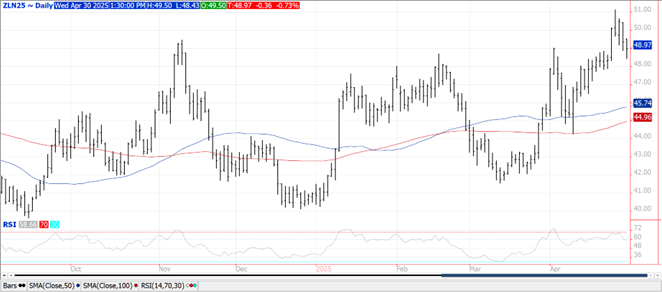

Prices finished lower across the soy complex today with beans down $.06-$.08, meal was slightly lower while oil was down 35-50 points. Spreads firmed in bean oil and were mixed in both soybean and meal. Deliveries against May beans were only 3 contracts, 629 for meal and 852 for oil. July-25 beans fell to a 2 week low however held support at its 50 day MA at $10.37 ¼. July-25 oil continues to fall back from recent highs over $.51 as still no indication the Trump Administration will extend the $1 per gallon blenders credit. With the Argentine bean harvest off to a very slow start, sales of this year’s crop sit at an 11 year low. That said at midday the RGE reported Argentine farmers sold roughly 230k mt of beans yesterday, the largest amount in the calendar year. News that China claims they can secure adequate agricultural supplies without having to rely on the US imports still seemed to weigh on the soy complex. China looks to expand the use microbial protein, food waste, insect protein and animal-based protein by 10 mmt by 2030. Bean oil used in the production of biofuels fell another 12% in Feb-25 to only 576 mil. lbs., the lowest in 5 years. It was also down 35% from Feb-24 as the market adjusts to the expiration of the blenders credit at the end of 2024. Usage over the first 5 months of the 24/25 MY at 4.746 bil. lbs. is down 7.3% from YA, vs. the revised USDA forecast of up 2%. Despite recent cuts by the USDA, their current usage est. for the 24/25 MY at 13.25 bil. lbs. is still too high unless the credit is reinstated. Combined biodiesel and RD production slipped 6% to only 319 mil. gallons, a 2 year low. Already released RIN data from Mch-25 suggests a sizeable production increase. Tomorrow’s census crush is expected to show nearly 206 mil. bu. were processed in Mch-25, which if realized would be a record high for the month. Export sales are expected to range from 5-25 mil. bu. of beans, 150-450k tons of meal, and 5-30k tons of oil.

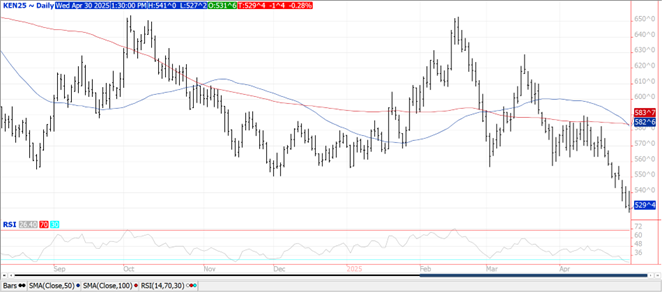

Prices were mixed ranging from $.02 lower in KC to $.04-$.09 higher in CGO and MGEX. KC was not able to hold the morning rally, likely the result of month end speculative short covering. Spreads firmed across all 3 classes. Early trade saw fresh contract lows for July-25 CGO and KC futures, the 3rd consecutive day for both. Perhaps too much rain across key US winter wheat growing areas is fueling quality concerns. Heavy rains were recorded across NC TX and OK the past 24 hours with more on the way. Over the next week we could see some localized flooding across the S. plains but we’ll definitely see further easing of drought conditions. Net drying across EC China may pose a late threat to their winter wheat crop. The USDA is currently projecting record production at just over 140 mmt. The BAGE is projecting Argentina’s 2025/26 wheat production at 20.5 mmt, which if realized would be the 2nd higher ever. Russia raised their export tax 10% to 1,758 roubles/mt for the period ended May 13th. Export sales tomorrow are expected to range from 0-25 mil. bu.

Charts provided by QST.

>>See more market commentary here.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.