Written Commentary

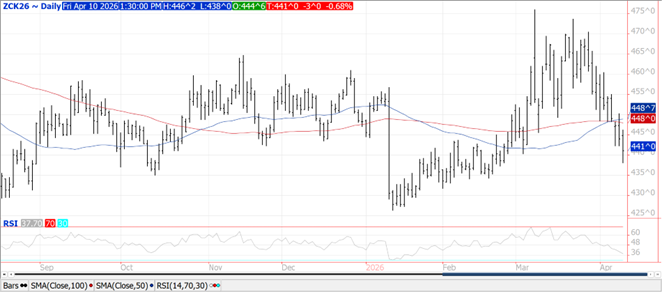

Prices were $.02-$.03 lower closing near the midpoint of the sessions range. Spreads were mixed. May-26 dipped to a 6 week low before recovering. Next support for Dec-26 is the 100 day MA at $4.67 ¾. The USDA did announce a flash sale of 126k mt (5 mil. bu.) of corn to an unknown buyer. No surprises in yesterday’s USDA WASDE report with US ending stocks holding steady at 2.127 bil. bu. Huge gap in Argentine production est. with the USDA at 52 mmt, the Rosario Exchange at 67 mmt, while the BAGE in between at 57 mmt. If their final production is closer to the RE estimate US corn will find much competition in Q4 of the 25/26 MY. Brazil’s 2nd crop prospects remain high. Argentine harvest has reached 22%. SovEcon lowered Ukraine’s production forecast 1.7 mmt to 28.1 citing fertilizer and fuel supply risks.

Sharply mixed trade across the complex with beans up $.05-$.10, meal surged $9-$14 while oil backed up 60 points. Bean and meal spreads were strong while oil spreads were flat. May-26 beans were not able to break out of its 4 week range between $11.40-$11.80. Resistance for Nov-26 beans is at $11.64. The surge in May-26 meal stopped shy of its March high of $335.50. Fueling the surge in meal prices were indications Iran is seeking meal from Brazil, a flash 100k tons US sale to Italy along with the Brazilian real surging to a 2 year high. For a change energy prices were reasonably quiet in 2 sided trade with no major developments in the US/Iran war. May-26 oil closed at about the midpoint of today’s range. Crush margins surged $.14 bu. to $2.92 with bean oil PV pulling back to 50.3%. No surprise the USDA held ending stocks steady at 350 mil. bu. Also surprised the increased meal supplies were absorbed via higher domestic usage while no increase to exports. Chinese weapons supplied to Iran could complicate negotiations. The BAGE kept Argentine production at 48.5 mmt, just above USDA’s 48 mmt forecast. This afternoon’s CFTC data will likely print out another record long by MM’s in soybean oil.

Prices ranged from steady in KC to $.07 lower in MIAX. Nearby spreads firmed while back months weakened. The 50 day MA capped the CGO July-26 rally attempt. KC July-26 for now rejected trade below $6.00. MIAX July-26 has fallen below its 50 day MA for first time in 2 months. US stocks were slightly above expectations at 938 mil. bu. The bearishness of yesterday’s 6 mmt increase in global supplies may be muted a bit by the fact most of the increase (4.8 mmt) occurred in India and not in traditional exporting countries. That said however, stock/use among exporting countries did jump to 18.2% vs. 17.7% last month, the highest in decades. While US WW areas in drought rose 3% LW to 68%, a fresh 52-week high, look for easing in future updates.

Charts provided by CQG

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.