Written Commentary

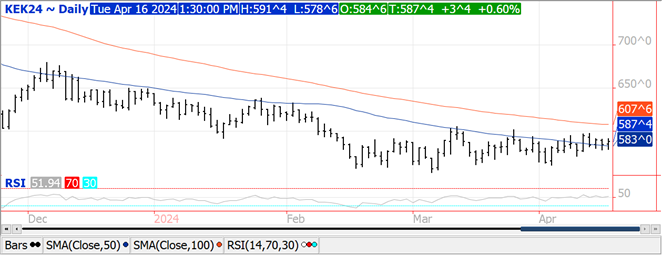

Prices were $.00 ½ – $.02 lower today with spreads firming on strong cash basis. May-24 remains stuck in a $4.24 ½ – $4.48 range. Dec-24 has yet to break out of the daily range from Mch 28th of $4.60 ¾ – $4.81. Showers have spread over the NW third of the US corn and soybean belt the past 24 hours with some areas picking up 2+” so far. Much cooler temperatures will fill in behind this system with overnight lows expected to dip into the mid 20’s this weekend for the Dakotas, along with parts of MN and northern NE. US plantings advanced only 3% LW to 6% complete vs. 7% YA and the 5-year Ave. of 6%. Plantings were at the low end of expectations. USDA Sec. Vilsack speaking yesterday in Washington DC remains hopeful the revised model to determine whether corn based ethanol will qualify for tax credits in the production of SAF will be announced by the end of April. Ukraine’s Ag. Ministry expects 2024 grain harvest will only reach 52 mmt, down from 58 mmt YA. They forecast corn production will reach 27 mmt, same as YA, however down from the USDA forecast of 29.5 mmt. Dr. Michael Cordonnier lowered his Argentine corn production forecast 3 mmt to 50 mmt, in line with the Argentine exchanges and well below the USDA forecast of 55 mmt. Tomorrow’s EIA report is expected to show ethanol production to range from 1,033 – 1,051 tbd last week, down from 1,056 tbd the previous week.

Prices were lower across the board today with beans down $.09 – $.13, meal was $2 – $3 lower, while oil was 50 – 60 lower. May-24 beans fell to a 6 week low with next support at the contract low of $11.28 ½. May-24 meal closed below its 50 day MA support at $336.60. May-24 oil also fell to a 6 week low with next support at its contract lows at 44.18. Not much change with SA weather however there does appear to be growing concern heavier than expected rains in Argentina over the past week may lead to some production losses or quality concerns with harvest being delayed. Australia’s weather bureau has declared El Nino conditions have ended however are not sure whether La Nina conditions will develop later this year. The Chinese economy grew 5.3% in Q1, above expectations for 5% growth and up from 5.2% in Q4 2023.Bean oil remains under pressure from yesterday’s bearish NOPA crush report showing higher than expected stocks despite crush coming in below expectations. Implied usage remains weaker than expected as biofuel manufacturers increase their usage of canola oil and used cooking oil. Yesterday afternoon the Rosario Grain Exchange warned recent heavy rains may lead to additional production losses due to delayed harvest and disease issues. Last week they lowered their production forecast to 51 mmt, vs. the USDA est. of 50 mmt. Dr. Michael Cordonnier raised his Brazilian production forecast 2 mmt to 147 mmt, just above Conab at 146.5 mmt, and below the USDA’s 155 mmt forecast. Crushing group Abiove raised their Brazilian production forecast to 160.3 mmt. US planting progress was reported at 3%, in line with YA and ahead of the 5-year Ave. of 1%.

Prices were little changed today with KC and MGEX up $.01 – $.03 while Chicago was $.02 – $.04 lower. Widespread rain is still lacking for much of western KN along with OK and TX panhandles for the next week to 10 days. Overall ratings remain the highest since 2020. Two states jump out, KS saw G/E ratings slip 6% to 43% G/E, while poor/VP increased 5% to 19%. Ratings in IL jumped 13% to 78%. 11% of the crop is headed, vs 9% YA and the 5-year Ave. of 7%. Spring wheat plantings advanced 4% to 7% complete, vs. 2% YA and 5-year Ave. of 6%. Ukraine’s Ag. Ministry forecasts 2024 wheat production at 19 mmt, below the 21.5 mmt YA and well below the USDA forecast of 23.4 mmt. Egypt’s GASC reportedly bought 120k mt of Ukrainian wheat at an average price just over $220/mt FOB. Freight costs were $35.35/mt. Russia was the 2nd lowest offer at $230/mt FOB for 180 day LC. Jordan didn’t buy wheat in their most recent tender.

Chart Source: QST

>>See more market commentary here.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.