Written Commentary

Prices were $.06-$.07 higher closing near session highs. Spreads were mixed. June 1st stocks at 5.295 bil. bu. implies March-May usage at a record 3.744 bil. bu. up 6.7% from YA, which should raise the price floor. 2026 acres however, still above 95 mil. may limit the upside unless US weather becomes more threatening or demand from China emerges. EIA data showed ethanol production rebounded to 1,117 tbd, or 328 mil. gallons last week, up from 320 mil. the previous week and up 3.8% from YA. Production was above expectations. There was 110 mil. bu. of corn used in the production process, or 15.66 mil. bu. per day, however still below 15.8 needed to reach the USDA forecast of 5.575 bil. bu. In the MY to date there has been 4.531 bil. bu. used, or 15.15 mbd, an annualized pace of 5.532 bil. Ethanol stocks increased to 24.7 mil. barrels, above YA at 24.1 mb. Implied gasoline usage rose 4% last week to 9.131 tbd, while up 5.7% YOY. Corn usage for ethanol production from May-26 at nearly 472 mil. bu. was above expectations and 6% above May-25. In the first 9 months of the 25/26 MY corn usage has reached 4.127 bil. bu., up 1.34% from YA vs. the USDA forecast of up 2.56%. To reach the current USDA est. usage in Q4 will need to reach 1.448 bil. bu. up 5.8% from YA. Tomorrow’s export sales are expected to range from 32-86 mil. bu.

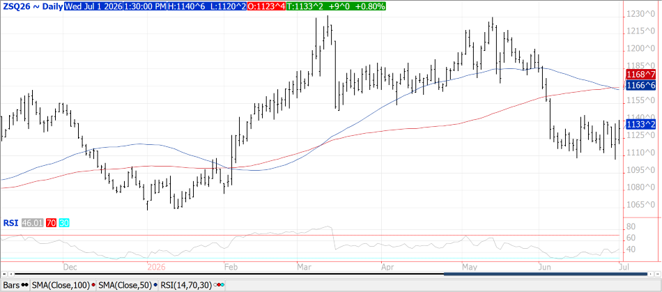

A late recovery in soybean oil enabled nearly the entire complex to close higher. Beans were $.05-$.10 higher, meal was up $1-$2 while oil ranged from 24 lower to 10 higher. Bean spreads firmed while product spreads were mixed. Aug-26 soybeans remain rangebound between $11.05-$11.45. Nov-26 beans stretched out to a 4-week high before pulling back. Next resistance is at $11.66 ¼. Aug-26 meal remains in a $300-$310 range. Aug-26 oil slipped to a 2 ½ month low before bouncing. Crush margins recovered to end only $.02 lower at $2.85 ½ bu. after plunging $.34 yesterday. US FOB offers at the Gulf are slightly below Brazilian offers Aug-26 forward. Yesterday’s USDA data was neutral for the complex with both stocks and acres close to expectations. Early weakness in bean oil was attributed to speculative selling, heavy deliveries and record canola acres in Canada. Also weighing on bean oil was EIA data that showed use for green diesel production fell 4.6% in April to 1.224 bil. lbs. well behind the pace to reach the USDA forecast of 14.550 bil. lbs. for the 25/26 MY. Bean oil usage as a feedstock fell to a 4-month low at 37.7% while tallow usage rose to 34.8% and UCO up to 14.5%. Tomorrow’s export sales are expected to range from 25-50 mil. bu. for soybeans, 150-500k tons for meal and 0-13k tons for oil. Census crush in May at 213 mil. bu. was slightly below expectations while bringing YTD crush to 1.997 bil. bu. up 8.2% from YA, vs. the USDA forecast of up 8.4%. To reach the current USDA forecast of 2.650 bil. bu. crush June thru Aug. will need to average 218 mil. bu. per month vs. 200 mil. YA. Bean oil stocks fell to 2.315 bil. lbs. however was nearly 100 mil. above expectations.

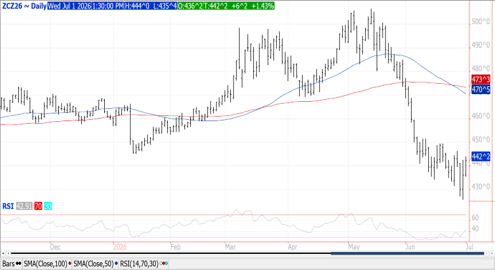

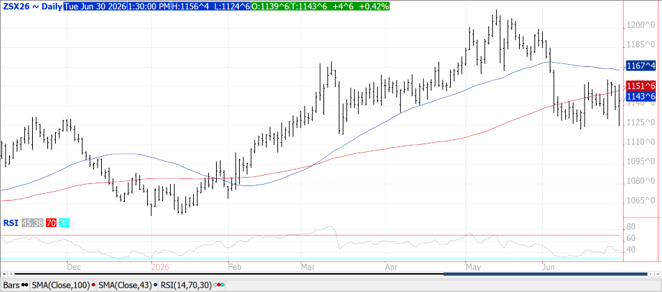

Prices finished $.10-$.12 higher across the 3 classes while spreads firmed. CGO Sept-26 was up $.10 ¾ at $6.00, KC Sept-26 was $.09 ¾ higher at $6.35 while MIAX Sept-26 was up $.12 at $6.18 ½. Lower wheat stocks combined with acres well below expectations has lifted the price floor for wheat. Winter wheat planted acres were cut another 890k to 31.52 mil. while harvested acres were down 805k to 21.21 mil. Using the updated acreage data and the state-by-state yield forecasts from June imply winter production at 1.002 bil. bu., down another 28 mil. Most of the acreage cuts came from HRW with OK down 300k acres, TX down 200k, KS down 100k and MT down 50k. Spring wheat acres were cut 25k vs. expectations for an 80k increase. At 9.39 mil. acres they are the lowest in 56 years. Despite speculative traders buying 8k contracts of CGO wheat yesterday, reducing their short position to 72K, open interest across all classes rose. CGO SRW OI rose over 7k contracts, 4k for KC HRW, and 2k in MIAX HRS. This was an indication of fresh $$$ coming into the long side of the market. Early thoughts on new crop endings stocks are just below 700 mil. bu. Export sales are expected to range from 10-20 mil. bu.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.